Singapore Airlines, our pride and glory. SIA has ranked among the best airlines in the world each year. Undoubtedly, it is one of the best investments made by the government, but is it a good investment for retail investors?

Here, we share our Singapore Airlines (SIA) stock analysis, take a look at their business, dividend history, latest financial year results, current SIA stock valuation and discuss if SIA is still a good Singapore blue-chip stock that you should invest in.

Singapore Airlines (SIA) Stock Analysis

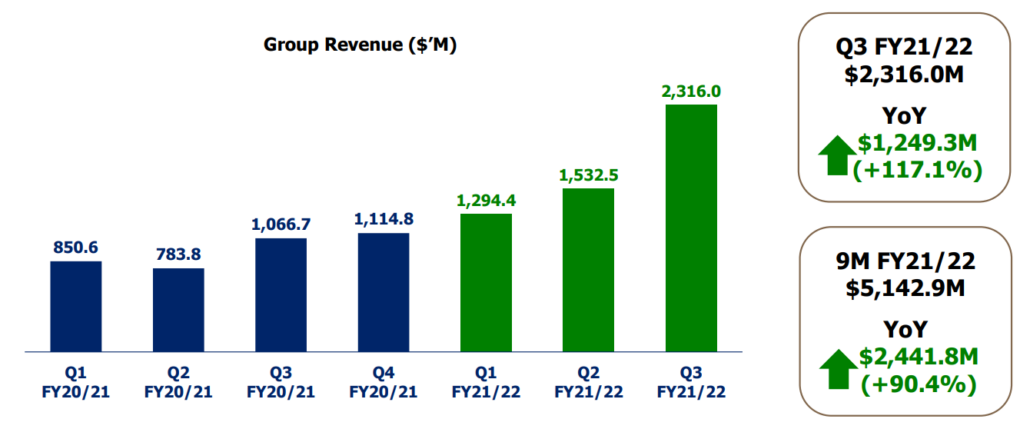

SIA announced its results Q3 FY21/22 report on 25 Feb 2022.

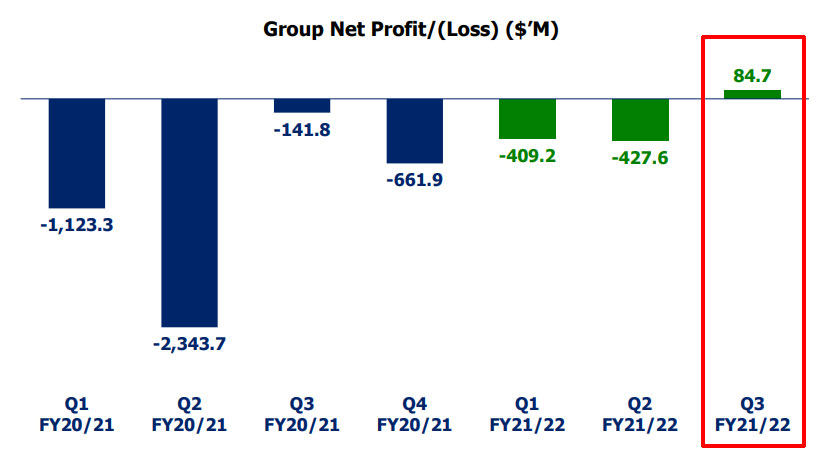

We are finally seeing the light at the end of the tunnel with SIA posting its first quarterly net profit of $85 million, since the pandemic. And as more vaccinated travel lanes open up, they are expecting to recover 51% of pre-Covid passenger capacity by March.

Revenue and Profit

As a result of border re-openings, SIA was able to increase revenue while minimising its net loss. Year on year, total revenue for Q3 FY 21/22 was up 117.1% at $2,316 million compared to just $1,066 million in Q3 FY 20/21.

And as mentioned above, SIA has posted its first quarterly net profit of $85 million, since the onset of Covid.

Revenue breakdown

Let’s look at how SIA’s revenue breakdown has changed since the pandemic. The left side displays a pie chart of SIA revenue breakdown for Q3 FY21/22. Cargo & Mail account for 58.3% of SIA revenue during this time, compared to 36% and 5.7% for passenger and engineering services, respectively.

On the right, the bar chart compares the company’s sub-segment to its pre-covid Q3 FY19/20 revenue. According to this graph, although Cargo & Mail grew by 258.5% while its passenger service, which was the main contributor to its income before Covid, is now only 22.7% of previous revenue.

Although the pandemic was a tough time, we got to give SIA some credit for being able partially generate revenue from cargo and mail. And as the world reopens, we should see their passenger segment recover in 2022.

However, SIA is not fully out of the woods yet as we have seen countries reverse their stance during the most recent Omicron outbreak.

Improving balance sheet

Its total debt climbed by $0.54 billion to $14.9 billion. Nevertheless, the Group’s debt-equity ratio declined from 0.90x to 0.67x, demonstrating an improvement from a debt standpoint.

Improving Cashflow

The cash flow of SIA is also improving. As of the latest financial report, SIA has achieved a surplus of $322 million in their 9M FY 21/22 operating cash.

SIA (C6L) Financials

SIA Dividend Yield

| Year | Dividend Yield (%) | Dividend Payout Per Share ($) |

|---|---|---|

| 2021 | 0% | $0 |

| 2020 | 0% | $0 |

| 2019 | 5.56% | $0.30 |

| 2018 | 7.04% | $0.38 |

| 2017 | 4% | $0.21 |

| 2016 | 8.15% | $0.44 |

| 2015 | 5.00% | $0.27 |

| 2014 | 7.59% | $0.41 |

| 2013 | 5.00% | $0.27 |

| 2012 | 2.96% | $0.16 |

Does SIA pay dividends in 2021?

SIA suspended their dividend pay out during the pandemic in order to conserve cash. They did not pay dividends in 2020 and 2021.

How much does SIA pay in dividend?

Prior to suspending dividends, SIA paid out $0.3 dividends per share in 2019, which worked out to be a yield of about 5.65%, based on share price in 2019.

How does Singapore Airlines make money?

Next, let us look at how SIA generates income.

To start, I used SIA’s FY19/20 revenue breakdown to get a sense of what a “normal” year would be like. COVID-19 had impact their performance since, but this would still provide a much more accurate portrayal of the company’s revenue breakdown after the pandemic comes to an end.

1. Passenger Service

Passenger services accounted for the majority of the company’s income before the pandemic, accounting for 80.5%. It is worth noting that SIA runs one of the world’s youngest fleets, with the average age of the entire SIA group being 5-6 years old. There are two sides to this coin. The negative side is that operating a younger fleet would result in higher capital expenditure since it would constantly need to refresh its fleet. On the other hand, a younger fleet could result in more cost savings from fuel-efficient planes and a more pleasant journey for passengers, which may benefit the firm in the long term.

The Passenger Service is further subdivided into two parts. Scoot and Singapore Airlines*. Singapore Airlines is the flagship carrier, linking Singapore to the rest of the world, while Scoot is a low-cost airline that mostly serves Asia and Australia.

* As of January 2021, SilkAir has officially merged with Singapore Airlines, which marks the end of the Singapore Airlines regional wing.

2. Cargo & Mail

SIA Cargo & Mail, which previously contribute a small portion of the company’s total revenue, has been a lifeline for the company during the pandemic, contributing 66.3% of total revenue, up from 12.2%. This growth is mainly due to the steep decline in passenger flights, but can also be attributed to the management decision to convert passenger aircraft for cargo deliveries.

Currently, SIA Cargo & Mail transport a diverse wide array of products worldwide, including fresh groceries, chilled meat, personal protective equipment, medical supplies, and pharmaceuticals.

3. Engineering Service and others

SIA Engineering Company is a subsidiary of SIA that provides maintenance, repair, and overhaul (MRO) services at 30 airports in seven countries. Unfortunately, the drop in operational flights during the pandemic has impacted its business since fewer aircraft are being serviced.

Why did SIA share price drop?

Operating an airline costs a lot of money. SIA’s share price dropped during the pandemic because countries were closing their borders and leisure travel was mostly shut down.

SIA has gone through many rounds of debt and stock financing during the pandemic to remain afloat, with the most recent issuance on 19 January 2022 where the corporation issued US$600 million of 3.375 % notes due in 2029.

Other notable capital raising over the past can 2 years are listed below. If you are interested in seeing how such capital raising has affected SIA valuation, check out our analysis:

- May 2020 – $8.8 billion of rights shares and Mandatory Convertible Bonds (MCBs)

- November 2020 – $850 million of convertible bonds

- November 2020 – $500 million from private placement bonds

- June 2021 – $6.2 billion of MCBs

Will SIA stocks recover?

tl;dr, SIA does look like it is on the road to recovery.

SIA publishes monthly operating statistics of the Group on its investor relation website and SGX portal, so you can check that out if you are vested in this company. The most recent one is its February 2022 operational results.

Based on the company’s most recent operational results, we see that SIA’s passenger capacity has recovered to 44% of its pre-Covid 19 levels in February 2022. This is likely to increase going forward as Singapore slowly reduces the cap on Vaccinated Travel Lane (VTL) daily arrival quota.

In the coming weeks, SIA will be expanding its VTL network, flying to a total of 66 cities in 27 countries. They also expect more VTL flights to be added progressively and expects passenger capacity to reach about 57% by April 2022.

Potential Risk: Rising Jet fuel costs

As we recover from the pandemic, SIA find themselves fighting another headwind. The spike in oil prices is a major concern for the company.

With the recovery of demand from international economies, we are currently experiencing a global energy crisis, with oil prices surging above historical highs. On top of that, inflation threatens to increase their operating cost.

Net fuel cost rose by 131.6% in Q3 FY21/22 as compared to the Q3 FY20/21. If this trend continues, it may further squeeze SIA’s already thin margins, slowing its recovery.

Is SIA overvalued?

To determine if SIA is overvalued, there are a few valuation ratios we could use. At the point of writing, these ratios suggests that SIA is still overvalued.

- Price / Earnings: -4.8

- Price / Book: 1.04

That said, it might not make sense to use Price/Earnings or Price/Cash ratios now because SIA has been losing cash in the past 2 years. You might also choose to use price to book ratio, but I prefer not to use it because SIA’s book (aka assets) depreciates rapidly, unlike properties.

Enterprise value to earnings before interest, taxes, depreciation, and amortisation (EV/EBITDA) ratio is another frequent multiple used to evaluate an airline. We will be able to eliminate non-cash elements from the assessment using this ratio, which is typical for the airline business with substantial capital expenditure, offering a more accurate and comparable metric.

Unfortunately, this value is likewise negative. Therefore, it does not function properly. If we utilised the trailing twelve months, we would generate a positive figure, but its multiple would be absurdly high, so there would be no use.

I believe the best way to value this company right now is based on its future profits.

What do you think SIA’s profits will be in a year? Do you think it’ll be able to recover completely? If you believe this then based on its current price, it has a chance to rebound to its pre-pandemic price of roughly $6.40 (adjusted for MCB dilution), which is about 20% upside from here.

But it is a huge if.

As the world has been confronted with new variants, we have been alternating between opening up and shutting down. Is this the last of such draconian border controls? That is anyone’s guess.

Is SIA stock a buy now?

With all that said about SIA, is its stock a good investment right now?

Singapore Airlines has evolved into more than simply a profit-maximising enterprise. It is of national importance and has brought about numerous intangible benefits, which have been and will continue to be considered in its business strategy moving forward. While such decisions are beneficial to Singapore, they may not translate into shareholder returns, even if the firm enjoys substantial government support via Temasek.

As the world gradually opens up again and returns to normalcy, the industry will recover. I have no doubt that Singapore Airlines will outperform its rivals in this region since it has used the pandemic to strengthen its operations.

SIA stock price may begin to rebound from here. Nonetheless, SIA operates in a highly competitive market with small margins, making it an unattractive investment.

Are you looking to invest in SIA? Share your thoughts in the comments below!

Frequently Asked Questions (FAQs)

Q: How to buy Singapore Airlines stock?

Singapore Airlines Limited (SGX:C6L) is listed on the Singapore Exchange (SGX), where the minimum lot size is 100 units. You can buy SIA stocks through:

- Stock Brokers: You can buy SIA’s stocks via any stock broker that gives you access to the Singapore stock markets.

- CPF Investment Scheme: At the point of writing, Singapore Airlines is a stock under the CPFIS. This means that retail investors in Singapore can also choose to invest in SIA via the CPF Investment Scheme.

Q: Who are the major shareholders of Singapore Airlines?

| Top 10 Shareholders of SIA (as of 31 Dec 2021) | Number of shares owned | % Shareholding |

|---|---|---|

| 1) Napier Investments Pte Ltd | 985,959,900 | 33.23% |

| 2) Temasek Holdings (Private) Ltd | 657,306,600 | 22.15% |

| 3) Citibank Noms Spore Pte Ltd | 170,238,981 | 5.74% |

| 4) DBS Nominees Pte Ltd | 134,348,142 | 4.53% |

| 5) Raffles Nominees Pte Ltd | 83,925,125 | 2.83% |

| 6) HSBC (Singapore) Nominees Pte Ltd | 70,630,404 | 2.38% |

| 7) DBSN Services Pte Ltd | 69,320,483 | 2.34% |

| 8) UOB Nominees Pte Ltd | 45,120,737 | 1.52% |

| 9) Phillip Securities Pte Ltd | 21,761,651 | 0.73% |

| 10) OCBC Singapore Nominees Pte Ltd | 17,641,120 | 0.59% |

Together, Singapore Airlines’ top 10 shareholders command 76% of the total shareholdings. However, do note that many of the shareholders are actually institutes that hold the shares for its nominees.

P.S. want to learn to valuate stocks independently? We teach our framework at this live Value Investing workshop.

worth buying SIA Engineering