Have you ever been asked this question when you tell someone that you are an investor in the stock market?

“Aren’t there many professionals out there who dedicate their lives to the stock market in this area? What makes you think you can beat those guys at their own game?”

Says everyone I have ever met

I know I’ve been asked this question countless times, albeit with certain words being paraphrased.

However, the main message is clear.

Can the average retail investor beat the pros at their own game ?

In One Up on Wall Street, the legendary investor, Peter Lynch, revealed how his ‘amateur’ approach in managing Fidelity’s multibillion-dollar Magellan Fund led him to become one of America’s number one money managers, and, one of the most successful investors of all time.

The Peter Lynch Investing Playbook is essentially a guide inspired by the book, One Up on Wall Street, where the legendary investor, Peter Lynch, revealed how his ‘amateur’ approach in managing Fidelity’s multibillion-dollar Magellan Fund led him to become one of America’s number one money managers, and, one of the most successful investors of all time.

From May of 1977 through May of 1990 Lynch captained Magellan to an annualized return of 29.06% compared to just 15.52% for the S&P 500. To contextualize things, let us see the returns one would have if you invested $1 in Magellan and $1 into the S&P 500.

His mantra is simple:

Average investors can become experts in their own field and can pick winning stocks as effectively as Wall Street professionals by doing just a little research.

In this colossal article, I hope to break down the key takeaways I’ve gotten from Peter Lynch’s book , namely – Peter Lynch’s general guidelines to stock investing.

The lessons taught by Peter Lynch can be broken down into 5 simple takeaways:

- Why retail investors have an edge over the Pros

- The psychological aspect of Stock Investing

- Traits of the “Tenbagger” (Wall Street Lingo for when you 10x your money)

- The Red Flags in the Market

- The Perfect Stock! I found it! I found it! Now What? (The checklist)

Why Retail Investors Have An Edge Over The Pros

Dumb money is only dumb when it listens to the smart money

Peter Lynch

The very first rule preached by the book is for one to stop listening to professionals!

That means ignoring the hot tips, the recommendations from brokerage firms and the latest “can’t miss” suggestion from your favourite newsletter – in favour of your own research.

In fact, the amateur investor has numerous built-in advantages that, if exploited, should result them outperforming the experts, and also the market in general.

This is due to the following factors:

- Size

- Safe Playing

- Capital is dependent on clients

- Street Lag

- Our On-The-Ground Expertise

1: Size

“If I was running $1 million today, or $10 million for that matter, I’d be fully invested. Anyone who says that size does not hurt investment performance is selling. The highest rates of return I’ve ever achieved were in the 1950s. I killed the Dow. You ought to see the numbers. But I was investing peanuts then. It’s a huge structural advantage not to have a lot of money. I think I could make you 50% a year on $1 million. No, I know I could. I guarantee that.”

Warren Buffett’s sharing on June 23, 1999 during Business Week

The professionals have very deep pockets due to their access to large sums of capital. This, however, puts them at a disadvantage as they are unable to invest in small to medium market cap stocks. It simply would not have a meaningful impact on the funds overall performance.

This was why Warren Buffett transitioned from investing in small cigar stocks to buying over whole companies later on.

The opportunities available to the average retail investors are much more than that for large investors. It is like picking from an ocean of fish compared to fishing in Pasir Ris pond.

We just need to capitalize on it.

2: Losing Small vs Winning Big

“You’ll never lose your job losing your clients’ money in IBM”

Peter Lynch

Between the chance of making an unusually large profit on an unknown company and the assurance of losing only a small amount on an established company, the professionals would jump at the latter.

Success is one thing, but it’s more important not to look bad when you fail. This is because fund managers are employees and their job would most likely depend on their performance.

Clients would rather hear the news that they lost small in DBS or Keppel versus winning big in Goodland Group Ltd.

Meanwhile, for the average person, there is no one calling us early in the morning or late into the night to drill us on why we bought a not-so-well-known counter.

We make our own decisions without having to prepare a 20-minute long explanation script to face potential backlash.

Peter Lynch thus encourages us to capitalize on such advantages to perform in the market as we are able to utilize our time more productively.

Worst of all, in the unfortunate event the stock tanks, no one would be there to criticize your prior judgement which might affect one’s investment decisions and actions.

3: Pros’ Capital is Dependant on Clients

Due to the fact that fund managers manage other people’s money, it is the clients that decide how much capital these fund managers have at their disposal.

These people aren’t usually savvy investors and tend to pull back their money during a bear market and put back their money during bulls. This is exactly the opposite of what one should do. This leaves the fund manager with the dilemma of having too much capital when everything is too expensive and too little when everything is selling cheaply.

Meanwhile, we are our own fund managers and we have the sole power to decide when to put-in and pull-out our capital. This gives us a key advantage should we meaningfully strategize our capital.

There would be no one calling you to pull out your capital when the stock tanks other than your weak heart which you must learn to ignore. (Lynch places a huge importance on the psychological aspect, which would be covered in the next section)

4: Street Lag

Under the current system, a stock isn’t truly attractive until a number of large institutions have recognized its suitability and an equal number of analysts (the researchers who track the various industries and companies) have put it in the buy or add list.

This means that by the time the stock’s analysis report is released, one should be sure that the smart money has already bought the stock at much cheaper and attractive prices as compared to the price they are currently reporting.

Therefore, it is better to not rely on such “buy” or “add” reports released to identify their stocks and should rather screen for their own stocks with one’s own criterion.

This is also due to the fact that such analysis reports have shorter term horizons compared to your own investing horizon. Analysts base their ratings of stocks on price targets they set and usually, these targets are provided in a 12-month(1 year) time frame.

For investors (not swing-traders), owning a stock for a single year is fraught with risk.

Behavioural economists De Bondt and Thaler came to the realisation that people do not make decisions rationally. Their decisions were distorted by the vast amount of cognitive errors they have to contend with.

Thus, having a one year holding period exposes the investor to market fluctuations as it takes time for the market to eventually function as the proverbial weighing machine.

Read more about holding periods in our Factor-Based Investing Guide.

5: Our On-The-Ground Expertise

“The best place to begin looking for the ten-bagger is close to home – if not in the backyard then down at the shopping mall, and especially wherever you happen to work”

Peter Lynch

We all have the chance to say, “This is great; I wonder about the stock” long before the professional analysts got its original clue.

We all have certain industries, products and services that we know more about than the average person does. Perhaps you know more about the gaming industries because you are a level 99 magician ninja and dominate every game you touch. Perhaps you are working in the fashion industry and are in sync with the latest trends.

Lynch states that the average person comes across a likely prospect two or three times a year – sometimes more.

The bottom line is that we all have valuable and relevant information on publicly listed companies through our everyday lives. This is information that the professionals either do not know about yet or have spent 100 hours of research to attain.

The psychological aspect of Investing

Human emotions make us terrible stock market investors, Peter Lynch states.

The ignorant investor continually passes in and out of three emotional states:

- Concern

- Complacency

- Capitulation (the action of ceasing to resist)

He/She is concerned after the market has dropped or the economy has seemed to falter, which keeps him/her from buying good companies at bargain prices

Then, as the next bull run arrives, he/she re-enters at higher prices and gets complacent because their holdings are going up. This is precisely the time he/she ought to be concerned enough to check the fundamentals vis-a-vis the current price, to determine whether it is overvalued and inflated (but he/she doesn’t).

Finally, when his/her stocks fall on hard times and the prices fall below what he/she paid, they capitulate and sells in a snit.

Many people term themselves as “Long-Term Investors” but only until the next big drop (or tiny gain), at which point they quickly become short-term investors and sell out for huge losses or the occasional minuscule profit.

The trick is not to learn to trust your gut feelings, but rather to discipline yourself to ignore them. Stand by your stocks as long as the fundamental story of the company hasn’t changed.

Lynch promises that if you ignore the ups and downs of the market, and the endless speculation on interest rates, in the long term, your portfolio will reward you should you make the correct selections fundamentally.

Even one of Warren Buffet’s greatest ever long term investments (Washington Post) looked like a complete loser for the first few years.

The Washington Post’s stock tanked by around 20% after Buffett’s purchase and had remained there for three years! That was a paper-loss of around $2.2 Million dollars. However, Warren revisited the financial statements and found out that there was no significant change in business fundamentals. He thus decided to hold and wait for the market to realize the Post’s true value. By the end of 2007, his stake in the Post had grown to US$1.4 Billion which is a gain of more than 10,000%.

Stocks with great long term returns can be really agonizing investments over the short term.

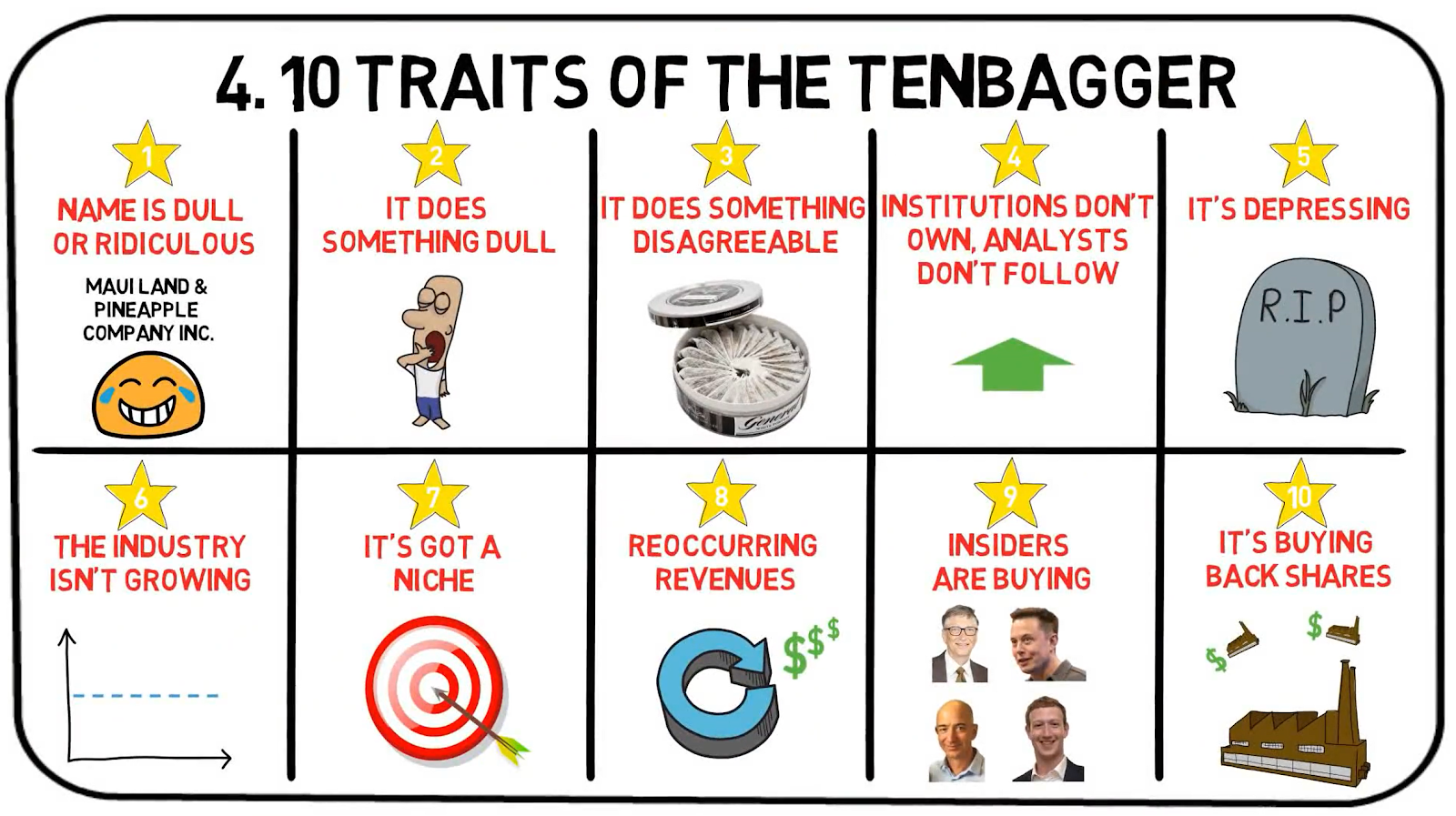

Traits of the “Tenbagger”

The legendary ‘Tenbagger’ is the expression Lynch uses to describe a stock that has appreciated tenfold your purchasing price. In One Up on Wall Street, he lists down several traits that such Tenbaggers should encompass.

In his book, Peter Lynch comes up with the Greatest Company Of All – An Ideal Lynch Tenbagger.

This mythical company is named Cajun Cleansers.

It was the magical company Peter Lynch described in the chapter about attributes of a dream enterprise.

Cajun Cleansers is engaged in the boring business of removing mildew stains from furniture, rare books, and draperies that are victims of subtropical humidity. Not one analyst from New York or Boston ever visited Cajun Cleansers, nor has any institution bought its shares.

Mention Cajun Cleansers at a cocktail party and soon you’ll be talking to yourself. It sounds ridiculous to everyone within earshot.

While expanding quickly through the country, Cajun Cleansers has had incredible sales. These sales will soon accelerate because the company just revealed a patent on a new gel that removes all sorts of stains from clothes, furniture, carpets and bathroom tiles. The patent gives Cajun the niche it’s been looking for.

The company is planning to offer lifetime prestain insurance with annual installments, who can pay in advance for a guaranteed removal of all the future stain accidents they ever cause on any surface.

The stock opened at $8 in an IPO seven years ago and soon rose to $10. At that price the important corporate directors bought as many shares as they could afford.

I visit the company and find out that any trained crustacean could oversee the making of the gel.

While Cajun Cleansers is a fictional business, you can have a sensing of what a tenbagger looked like in the eyes of the legendary Magellan fund manager. The aforementioned story description is not too far off the business models and existing environments of several companies in our midst.

The Red Flags in the Market

“If I could avoid a single stock, it would be the hottest stock in the hottest industry, the one that gets the most favourable publicity, the one that every investor hears about in the carpool or on the commuter train- and succumbing to social pressure, often buys”

Peter Lynch

Hot stocks can go up fast, usually out of sight of any known landmarks of value, but since there’s nothing but hope and thin air to support them, they fall just as quickly.

Let us take a look at Best World, a hot stock that tumbled after Bonitas Research published a 28-page report that questioned the authenticity and legality of the premium skincare firm’s profits.

Other than the sexiest stock in the hottest industry, here are 4 other traits of the stocks Peter Lynch would definitely avoid:

- The “Next Amazon”, The “Next Facebook” and the “Next Google”

- DiWORSEifications

- The Whisper Stock

- Reliant on a single/few customers

1) The “Next Amazon”, The “Next Facebook” and the “Next Google”

Beware when someone terms the stock as the next “Facebook” or the next “Google” because it is almost never is.

In fact, these are merely marketing tactics and click baits tactically placed to entice you to read on further.

“This stock, company ABCXYZ, could be like buying Facebook for $2 a share”

More often than not, they liken such stocks to the big players to make it relatable and to attract the ignorant investors who buy on hearsay.

This, in turn, entices them and the next thing you know, he commits half of his savings for retirement into buying shares of ABCXYZ, smugly touting to his friends that he got on the boat early.

2) Avoid Diworseifications

Some call it diversification, but Lynch likes to term bad decisions as Diworseifying.

Instead of buying back shares or raising dividends, profitable companies often prefer to blow their money on foolish acquisitions.

More often than not, one must ask themselves whether the company’s expansion is related to the core operations.

A few fictional (exaggerated) examples would include:

- Genting Singapore acquiring ST Engineering

- DBS buying over Koufu

- Singtel taking over Sheng Siong

Now, that would sound silly, leaving you wondering to yourself how the idea of such acquisitions managed to pass through the vetting of the management and leadership. The hard truth is that such lousy expansions exist.

If we draw upon people’s painful lesson of Hyflux, we could evidently see a jarring case of diworseification as the company expanded from innovating water solutions to generating power and energy.

Being the first in Singapore and Asia, the Tuaspring Integrated Water and Power Project was expected to raise efficiency levels and reduce the cost of desalination.

The power plant was opened in 2016 and it was Hyflux’s first venture into the energy business.

Notice how Hyflux chooses to report their profits and earnings by excluding Tuaspring?

This was because Tuaspring was a drag on the company’s earnings and profits, Hyflux stated that the “prolonged weakness” in the local energy market as one of the main reasons for its losses.

Read more about that fateful lesson here.

3) Avoid Whisper Stocks

These stocks are termed as the “Longshots”.

They are often thought of as being on the brink of doing something miraculous such as curing every type of cancer, solve global warming or create world peace.

Whisper stocks have a hypnotic effect, and usually the stories have emotional appeal. This is where the sizzle is so tantalizing that you forget to notice there’s no steak.

Sounds a whole lot like a MLM scheme where the Moringa Elixir promises to solve any kind of illness…

What all these longshots had in common besides the fact that you lost money on them was that it had a great story with no substance.

4) Avoid Businesses Reliant on a Single/Few customers

The company that has 25 – 50% of its sales reliant on a single customer is in a precarious situation.

If the loss of one customer would be catastrophic to a supplier, having a huge toll on its top line, Lynch would be wary of investing in the supplier.

In 2018, AEM Holdings was heavily reliant on its one major customer, while not specifically identified by the company, is believed to be Intel, one of the largest chip makers in the United States, which contributed around 93% of total revenue

This is also a weak bargaining position to be in and the company could potentially be squeezed by this only customer and be subjected to its influence.

I found it! I found it! Now What? (The Lynch checklist)

In the final chapters of the book, Lynch discloses a summary checklist of some (not all) of the important things he’d like to learn about stocks before delving deeper.

- The p/e ratio. Is it high or low for this particular company and for similar companies in the industry?

- The percentage of institutional ownership. The lower, the better.

- Whether insiders are buying and whether the company itself is buying back its own shares. Both are positive signs.

- The record of earnings growth to date and whether the earnings are sporadic or consistent. (The only category where the earnings may not be important is in the asset play.)

- Whether the company has a strong balance sheet or a weak balance sheet (debt-to-equity ratio) and how it’s rated for financial strength.

- The cash position. With $16 net cash, I know Ford is unlikely to drop below $16 a share. That’s the floor on the stock.

Don’t be confused by Peter Lynch’s homespun simplicity when it comes to doing diligent research – rigorous research was a cornerstone of his success.

When following up on the initial spark of a great idea, Lynch highlights several fundamental values that he expected to be met for any stock worth buying.

One Up on SGX?

As one would notice, Peter Lynch identifies a stock using Qualitative Analysis before diving into the Quantitative.

However, at Dr Wealth, we believe that one should perform quantitative analysis on a stock before dwelling into the qualitative.

That way, we can ignore any emotional biases which can do you harm.

We would like to highlight that both approaches would do the job, just remember not to forget either in your research.

All stock research is borne of a Quantitative and a Qualitative component.

We hope that you learnt something useful thus far. In the next few sessions, I’ll be diving into 3 stock categories that Peter Lynch used. They are:

- Stalwarts

- Fast growers

- Asset plays

Do note that Peter Lynch actually has 6 stock categories; Slow growers, Stalwarts, Fast growers, Cyclical, Asset plays, turnarounds.

Also, if you are as impressed and moved by America’s number-one money manager just as I am, you could consider purchasing his book. Kindle versions can be cheaper if reading books electronically is more your style.

By the way, we hold regular introductory courses to share our structured investing strategy. If you’d like to know how we have combined several of our own strategies to find our own growth stocks, you can learn more here.

Peter Lynch Stock Category 1: Stalwarts

Stalwarts are former fast-growing companies which have matured into larger companies with slower, more reliable, growth (3% per year is the expected average).

In addition, stalwart companies produce goods that are necessary and always in demand (think food, water, electricity, oil), which ensures a strong, steady cash flow.

Although they are not expected to be top market performers, if purchased at a good price, stalwarts offer significant profits of around 50% or so over a 4-5 year holding period.

Due to their strong cash flow generated from needed products, stalwarts are generally able to pay a dividend.

Examples of Stalwarts include Macdonald’s, SBS Transit, and Procter&Gamble.

In addition, Peter Lynch required Stalwarts to have a P/E growth ratio (PEG) of less than 1.0. The PEG ratio is calculated by dividing a company’s Price-to-Earnings (PE) ratio by its Earnings Growth Rate.

Lynch considered companies with PEG below 1.0 to be underpriced, and companies with a PEG of below 0.5 to be a real bargain. This is easy to understand, since if you buy a company with a PEG of less than 1, you are paying less than one dollar for a dollar of earnings growth. And paying less for more is the fundamental principle of all investing.

For dividend-paying companies, Lynch further factored in the dividend yield to arrive at a yield-adjusted PEG ratio. Walmart has often been cited as a good example of Lynch’s Stalwart stock methodology.

At a point in time, Wal-Mart traded for close to 20x PE. Which meant the average investor would be paying $20 per dollar of earnings.

Lynch determined that the company was still growing at 20-30% with much more room for growth.

This means the real price to earnings an investor would be paying would be 20-30% less every year for the next couple of years. $20 was a bargain. And Wal-mart did not disappoint, going on to grow at 20-30% for the next 20 years.

So How Do We Find Stalwarts?

We now know some of the characteristics of Stalwarts.

- A previously fast grower that has become a mature company, but with decent long term growth potential (3% per year)

- Produces needed goods/services that allow for strong cash flow generation

- Is able to pay a dividend and reward shareholders with that strong cash flow

- Has a PEG ratio of less than 1, or ideally less than 0.5

We have added some additional criteria to be extra stringent with our stock selection, and narrow our focus down to only the best stocks to be investigating. These are the final criteria for which we will be using to find Stalwarts in Singapore.

- Mid-Large Market Capitalization (above $80m Market Cap)

- High Dividend Yield (Within Top 50 Highest Div Yield stocks in SGX)

- Regular Dividend Distribution

- Earnings & Average Free Cash Flow > Dividends Distributed

- Increasing Revenue Growth Y-O-Y (Earnings calculated in Point 4)

- Not in a Sunset Industry (old & declining industry, for eg, textiles)

- PE ratio within Industry Average

- PEG ratio of less than one. Ideally 0.5 even.

The above criteria should be rather self-explanatory.

- Mid to Large Market Capitalisation means the company has achieved a certain level of scale and maturity in addition to being more liquid for investors.

- Higher Dividend Yield is a measure of squeezing out companies with less dividends

- Regular and Uninterrupted Dividend Distribution is a measure of a company’s ability to be financially disciplined and a reflection of its strong cash flow, which we covered earlier as necessary

- Think of free cash flow as a company’s savings after paying all of its bills for the month/year. If dividends exceed savings, the company has less cash in its account. Period. Repeat this for years straight and the company will go bankrupt much like Hyflux, which experienced 5 years of negative free cash flow.

- The price of a company in the stock market is often tied to its reported earnings. Good earnings see good appreciation in stock prices. So Increasing Top Line Growth Y-O-Y is necessary.

- Not being in a sunset industry should be self-explanatory. Sunset industries are dying trades. Such as shoe shiners. When was the last time you paid good money to have your shoes shined? Never? Well, now you know why I won’t invest in generic shoe-shining businesses. Low earnings reflect a lack of ability to pay dividends to shareholders, which naturally follows falling stock prices. Buying a stock in a Sunset industry would be like buying a dying puppy hoping it becomes a full-grown dog. Its the exact reverse of buying a growth stock.

- A PE ratio within the industry average means that the stock is not overvalued relative to its peers in the industry. This ensures we’re not overpaying.

- A PEG ratio of less than one. Ideally, even 0.5, which reflects that we’re paying less than a dollar for a dollar’s worth of earnings growth.

Given the above criteria, we shortlisted 3 Stalwarts that we will cover today, which we feel have significant growth potential. In addition, all of the stocks will have one or more of the following traits of a tenbagger, representing a potential return 10X of what you invested.

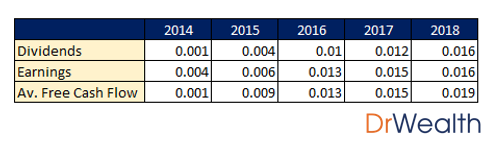

#1 – Jumbo (SGX:42R)

| Market Cap. | $253M |

| Historical Dividend Yield | 3% |

| Not in Sunset Industry | Yes |

| PE Ratio | 21.73 |

| Industry Average PE ratio | 23.8 |

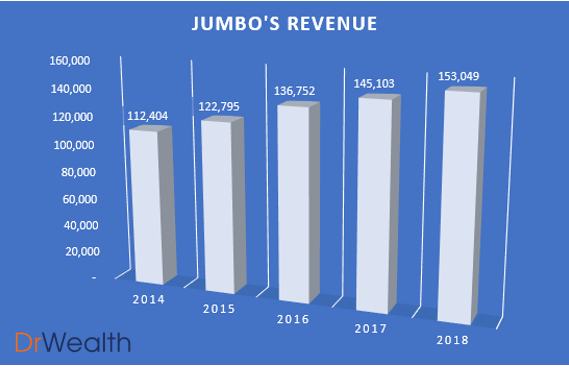

As seen in the chart, Jumbo’s revenue has been growing year on year with a 5% growth from $145m in 2017 to $153M in 2018.

We would also potentially expect the revenue growth to maintain or even increase as Jumbo looks towards gaining a firmer foothold in China and other regions.

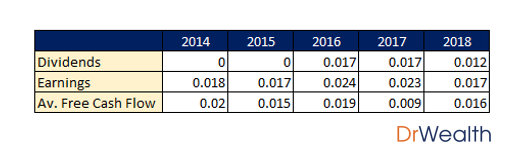

Jumbo has been distributing dividends for the past 3 years since its Initial Public Offering and its earnings and free cash flow has been more than the dividends distributed with the exception of 2017.

This was due to its unprecedented expansions into Beijing, Shanghai, Taiwan and Ho Chi Minh City. This does justify the fall in Free Cash Flow in 2017 and the subsequent fall in dividend distribution in 2018.

Jumbo’s Growth Potential

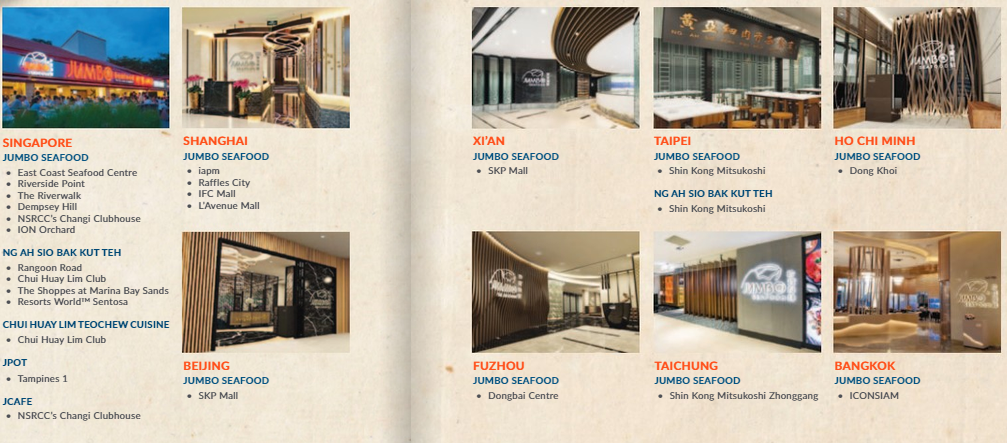

Jumbo aims to tackle its growth prospects with a three-pronged approach:

- Expanding to other F&B brands such as Ng Ah Sio Bak Kut Teh, JPot, Chin Hui Lim Teochew Cuisine and Tsui Wah cafe

- Identified PRC as a key growth market and ventured into China which has a much larger addressable consumer base

- Grew its franchising model throughout Asia – it has sprung up in Vietnam, Taiwan, Hong Kong, Korea and Bangkok

By diversifying its restaurant portfolio, it is able to replicate some parts of its successful seafood business model onto other brands such as Ng Ah Sio Bak Kut Teh. This could thus be another profitable venture for the group should they be able to execute it well. Jumbo intends to introduce Ng Ah Sio Bak Kut Teh to China and will open at least one more Ng Ah Sio Bak Kut Teh outlet in Taiwan and one more Tsui Wah Hong Kong-styled “Cha Chaan Teng” outlet in Singapore over the next 12 months.

Furthermore, by expanding into foreign consumer markets, Jumbo is exposed to a larger addressable consumer base.

Should they be able to build their brand as successfully as they have done in Singapore, there would be bright prospects ahead for the group.

The Edge Singapore just reported today that Jumbo opened its first franchised outlet in Gangnam, Seoul. This brings the tally of Jumbo seafood across Asia to 18 with franchised outlets in Bangkok, Fuzhou, Ho Chi Minh, Taipei and Taichung.

“We are enthusiastic about the opening of our first JUMBO Seafood restaurant in South Korea and to bring a part of Singapore’s heritage dishes to the country. We believe that the opening will strengthen the Group’s market position in the region, especially within North Asia, as we seek to steadily expand our network of F&B outlets.”

Ang Kiam Meng, Group CEO and Executive Director of JUMBO

Jumbo’s investment and expansion into China have begun to ripen as it currently accounts for approximately 20.4% of its Revenue. Such figures are a strong testament to its success in China.

Should the leadership and management build their market position within the different regions by expanding their outlets as successfully as it has done in China, we could potentially see unprecedented growth of the Company’s sales.

In the home base, which still forms the bedrock of the company’s earnings growth, Jumbo opened an outlet at ION Orchard.

This marks a significant milestone as their first restaurant in Orchard, the premium shopping and entertainment belt. This shows that while Jumbo is in the midst of overseas expansions, it still makes it a point to remain relevant and expand in the local market to maintain its main source of sales.

Peter Lynch’s Trait Checklist

It’s got a Niche

When you hear the name Jumbo, the picture that first pops into your mind is definitely a Chilli Crab/ Pepper Crab. That is exactly Jumbo’s Niche, selling one of Singapore iconic/ famed local dishes and being renowned for it.

Other than honing their Chilli Crab Expertise, having a Niche makes Jumbo very word-of-mouth friendly, which means more opportunities to get the word out about your business.

Having such a competitive advantage over its counterparts is important for restaurants like Jumbo which reside in a highly competitive F&B industry. This ensures that its sales would not be affected immensely in the presence of new seafood entrances due to high customer retention rates.

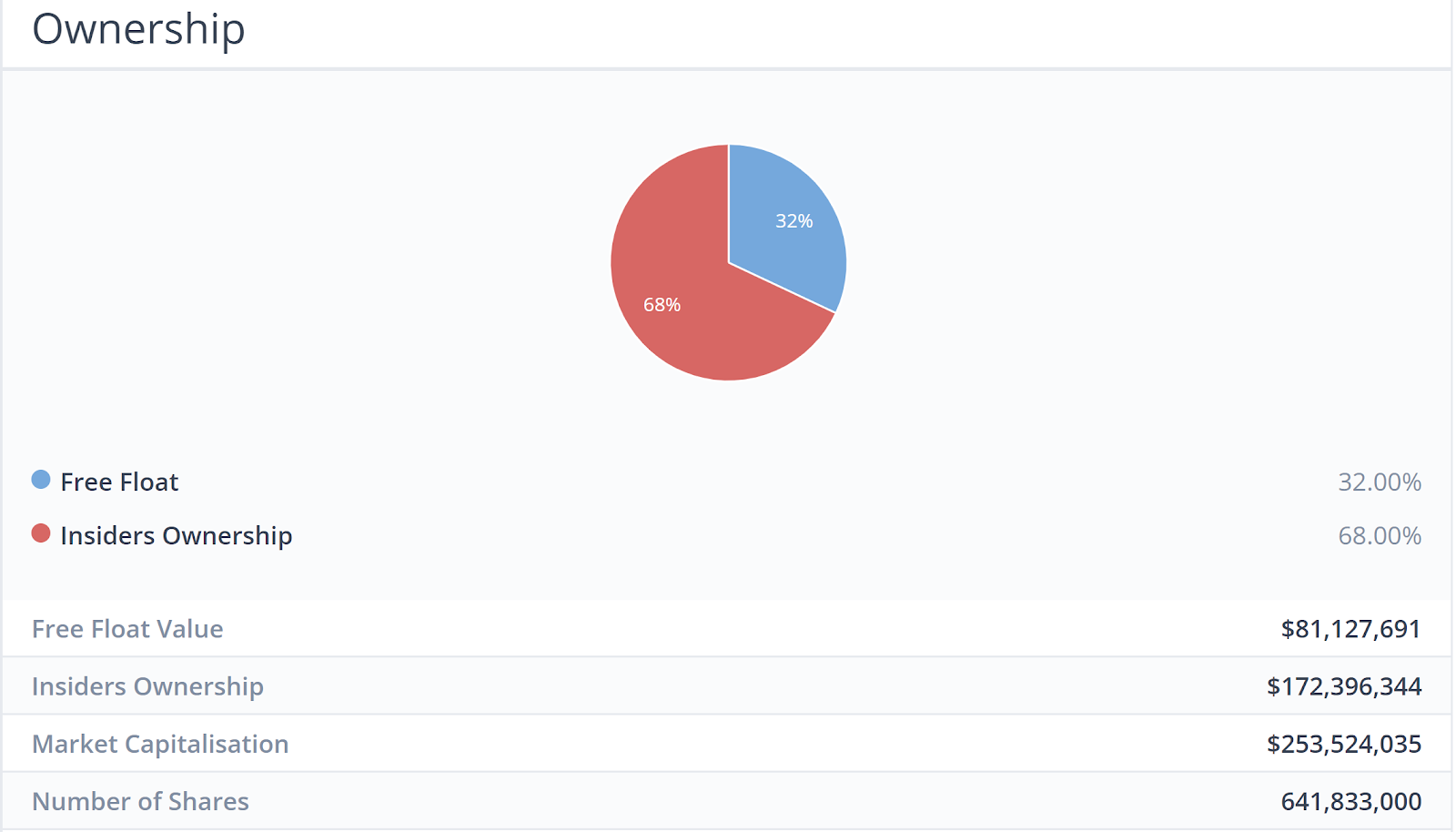

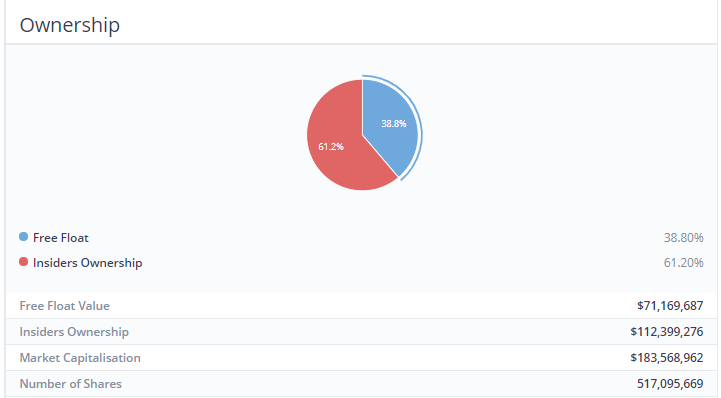

Skin in the Game (Insiders are buying/owning shares)

If the Chairman or the CEO of a company owns more than 50% of shares in the company, their interests are more likely to be more aligned with the shareholders.

That is because they are unlikely to take actions to harm their own wealth and would look towards improving the prospects of the company.

“There’s no probable success of stock than that people in the company are putting their own money into it.”

Peter Lynch

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

The Company is buying back Shares

Buying back shares is the simplest and best way a company can reward its investors, according to Peter Lynch.

If it has faith in its own future, then it would invest in itself, just as shareholders do.

“When stock is bought by the company, it is taken out of circulation, therefore shrinking the number of outstanding shares. This can have a magical effect on earnings per share, which in turn has a magical effect on the stock price.”

Peter Lynch

Jumbo has been doing just that, posting notices from 31st May – 11th June on their daily share buy-backs.

#2 – Japan Foods (SGX:5OI)

| Market Cap. | $81M |

| Historical Dividend Yield | 4.27% |

| Not in Sunset Industry | Yes |

| PE Ratio | 24.22 |

| Industry Average PE ratio | 23.8 |

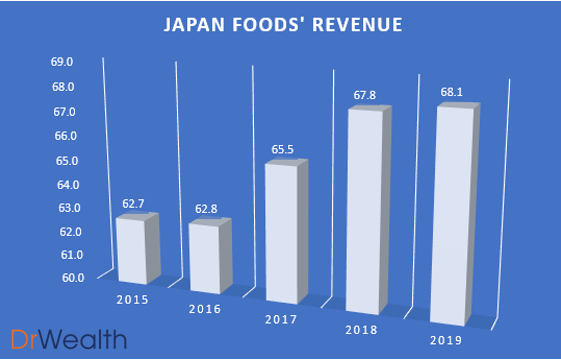

As seen in the chart, Japan Foods’ revenue has been growing year on year, albeit not substantially from 2018 to 2019. However, we would expect the top line to grow with the growth potential lined up for Japan Foods.

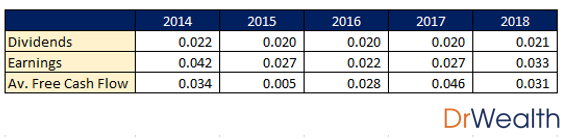

Japan Foods has been distributing consistent dividends for the past 5 years and its earnings and free cash flow has been more than the dividends distributed for all 5 years.

Japan Foods’ Growth Potential

Similar to Jumbo, Japan Foods business growth model focuses on three things:

- Expanding to other F&B brands (refer to the image below)

- Rejuvenating its oldest and most established brands to remain relevant

- Growing its franchising model throughout Asia – it has announced a 50-50 venture in Dec 2018 with Minor Food Group to expand into Japan, Thailand and PRC

Japan Foods’ approach moving forward seems logical and sound. Their joint venture under the franchise “Dining Collective” is a great leap forward in their overseas ambitions, allowing them to unlock a larger customer pool by expanding their outlets and having a presence in foreign markets.

They also managed to secure and launch a new franchised ramen brand “Konjiki Hototogisu”, known for its clam-flavoured broth. The restaurant chain also has One Michelin Star.

They have since opened four restaurants under this brand in Singapore, with the latest one being launched in Jewel Changi.

This is definitely not a form of diworseification as Japan Foods aims to tackle the premium market in Singapore whilst maintaining more affordable brands for the general crowd. This caters to the tastes and wallets of the consumers, unlocking more potential for growth.

Lastly, they launched two brand extensions of “Ajisen Ramen”, named “Den by Ajisen Ramen” and “Kara-Men”.

By refreshing and rejuvenating brands, it allows Japan Foods to remain competitive and relevant in the market. To date, the response to the two variations has indeed been well with an increase in same-store sales following the rebranding.

Peter Lynch’s Trait Checklist

It’s got a Niche

Lynch found that if a company focused on a particular niche, it often had little competition. Japan Foods is one of the leading F&B groups in Singapore specializing in Japanese cuisine. With 19 Dining Brands under their name and 50 locations islandwide, it seems that their restaurant network is stable and well-built.

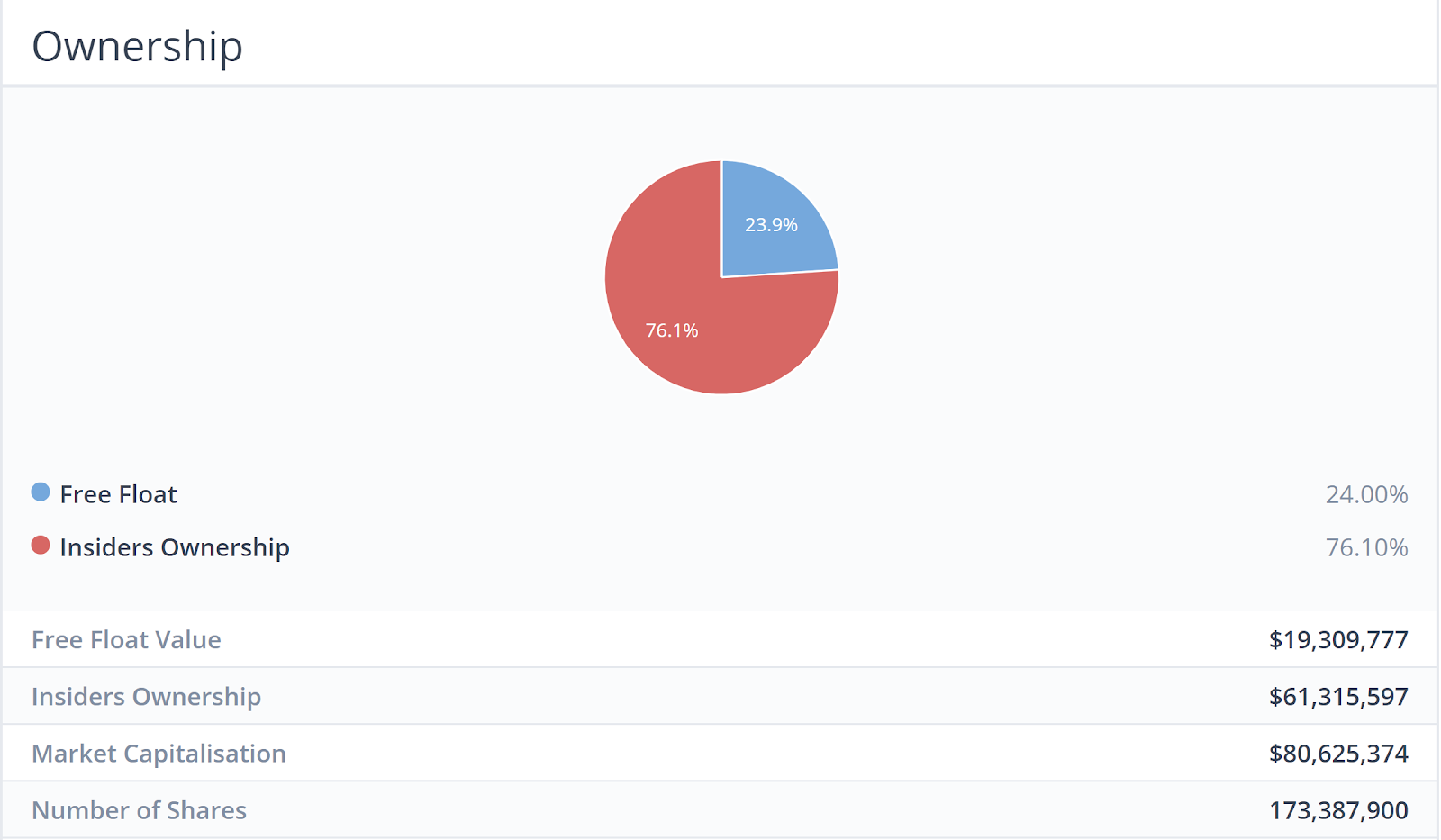

Skin in the Game (Insiders are buying/owning shares)

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

The Company is buying back shares

Japan Foods has also been posting notices in Aug 2018, Sep 2018, Dec 2018 and Feb 2018 on its daily share buybacks. Such notices can either be found on the SGX website or their investor relations website.

#3 – ISEC Healthcare Ltd (SGX:40T)

| Market Cap. | $186M |

| Historical Dividend Yield | 6.12% |

| Not in Sunset Industry | Yes |

| PE Ratio | 21.53 |

| Industry Average PE ratio | 47.95 |

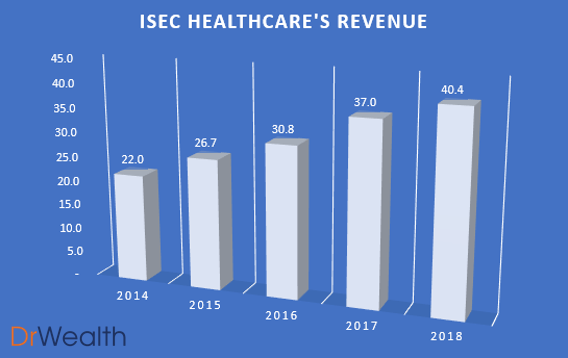

As seen in the chart, ISEC’s revenue has been growing year on year with a 9.19% growth from $37m in 2017 to $40.4M in 2018. We would also potentially expect the revenue growth to increase due to the region’s aging population and increasing awareness towards seeking early treatment for ophthalmology issues will continue to drive demand and sales upwards.

ISEC Healthcare has been distributing consistent increasing dividends for the past 5 years and its earnings and free cash flow has been more than or equal to the dividends distributed for all years.

ISEC Healthcare’s Growth Potential

We see growth potential in ISEC Healthcare’s business due to 3 key reasons:

- Ageing Population leading to greater demand for Eye Care

- Rising Income Levels and Private Insurance Covering leading to more affordable healthcare

- ISEC Healthcare’s regional expansion into larger population markets

Due to ageing populations, requirements for eye health care will increase. This is because there are higher incidences of Cataract, Glaucoma, Age Macular Degeneration, Dry Eyes and Vitreoretinal.

Furthermore, not only is government spending on healthcare services increasing across the region in line with changes in demographics, rising income levels and subsequent private insurance coverages has led to an increase in individual spending on private eye-care services.

ISEC Healthcare is also keen on regional expansions with large populations. They took a positive step towards this direction by announcing the incorporation of ISEC MYANMAR. They are also keen on leveraging upon the aforementioned trends to continue pursuing investment opportunities and explore up-and-coming markets such as China, Indonesia and Vietnam.

Peter Lynch’s Trait Checklist

It’s got a Niche

In terms of devising a business strategy, a niche company can remain focused on its area of specialization. Over time, a niche company can develop a reputation for its work in a given field. This reputation allows a niche company to position itself as a leader and expert in the field. Niche companies focus on doing one thing well rather than doing many things only adequately. ISEC Healthcare definitely has an Eye Specialist Niche. This gives it better margins as a specialist clinic than a generalist.

Skin in the Game (Insiders are buying/owning shares)

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

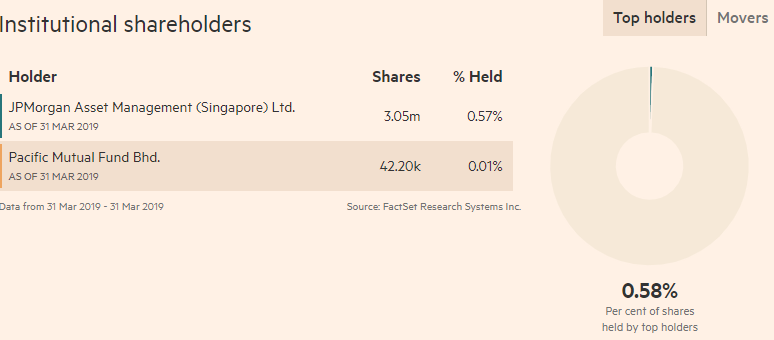

Not many Institutions own it

Peter Lynch states that if you find a stock with little or no institutional ownership, you’ve found a potential winner. Such companies have not been discovered by the smart money, giving it an extra potential upside.

So there you have it. The Stalwart Category explained in accordance with Peter Lynch’s guidebook.

Lynch expected stalwarts to deliver gains of 30% to 50%, after which he would sell them and find new, undervalued counters. These are the stocks that he would frequently replace with others in this category.

Next, we’re going in-depth into one of the six different categories pointed out by Lynch – The Fast Growers

Peter Lynch Stock Category 2: Fast Growers

These counters are among Lynch’s favourite investment. These stocks typically have the characteristics of small, aggressive new enterprises that grow at 20-25% a year. Lynch claims that if you were to choose these Fast Growers correctly, it could potentially be a 10 to 40 bagger.

We would be picking stocks utilizing the following criteria to select our Top 3 Fast Growers:

- Companies Earnings growth at least 20% over the past year

- Debt to Equity ratio less than 25

- Stable Revenue and Profit growth Y-O-Y

To elaborate a little further on the above criteria:

- Companies Earnings growth at least 20% over the past year means the company has achieved a certain level of growth versus prior year to be deemed as a “Fast Growers” as described as Peter Lynch.

- Debt to Equity less than 25. The debt-to-equity (D/E) ratio compares a company’s total liabilities to its shareholder equity and can be used to evaluate how much leverage a company is using. Higher leverage ratios tend to indicate a company or stock with higher risk to shareholders.

- Stable Revenue and Profit growth Y-O-Y is a measure of a company’s ability to be able to continue producing similar sustainable results in the long term.

At Dr Wealth, we believe that the Singapore Stock Exchange Market is more catered towards investors with the strategy of earning a passive income. Thus, while SGX is a fantastic market for dividend stocks/REITs there are much better growth stocks available beyond SGX.

We would, therefore, apply the aforementioned criteria in the US markets as we feel that growth stocks are aplenty there.

Given the above criteria, we shortlisted 3 Fast Growers that we will cover today, which we feel have significant growth potential. In addition, all of the stocks will have one or more of the following traits of a ten-bagger, representing a potential return 10X of what you invested.

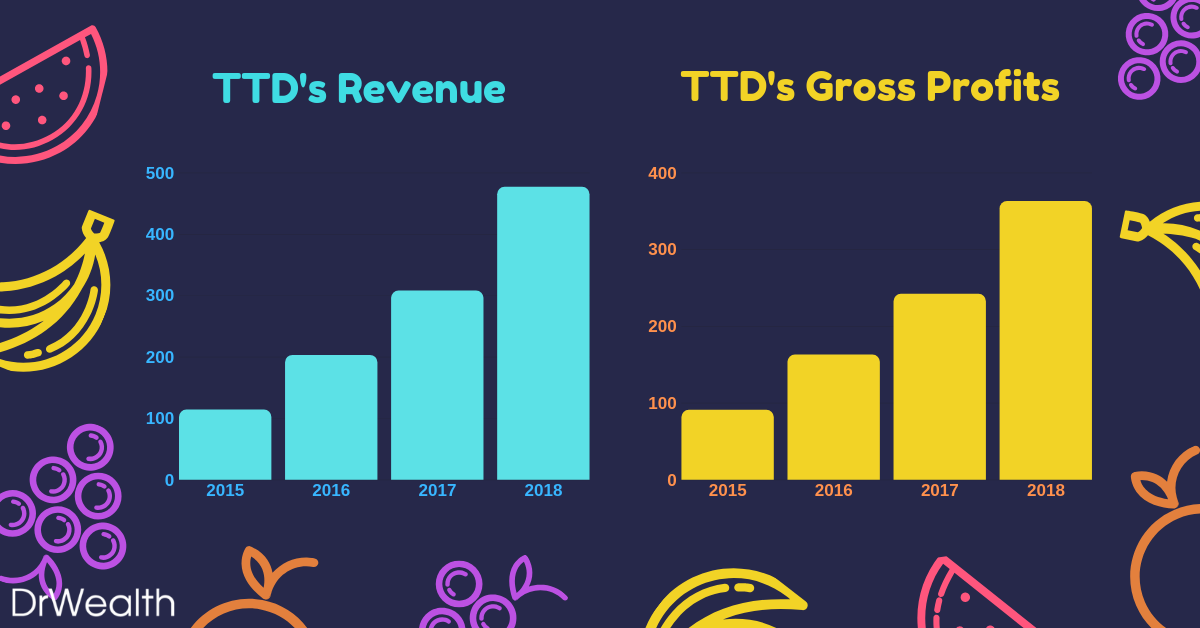

#1 – The Trade Desk (NASDAQ:TTD)

| Market Cap. | $11.62B |

| Debt-to-Equity Ratio | 18.54 |

| Stable Top & Bottom Line Y-O-Y | Yes |

As seen in the graph, The Trade Desk’s earnings have been growing year-on-year from 2015 to 2018. Earnings grew from $242M in 2017 to $363M in 2018, displaying a whopping 50.1% growth versus the prior year.

We would also potentially expect the earnings growth to maintain or even increase as The Trade Desk looks towards gaining a firmer foothold in China and other regions.

What does The Trade Desk do?

Do you realize that what you have searched on Google would start popping up in your Facebook/Instagram/Youtube feeds as adverts?

Eerily, most of the adverts are also very relevant to what you are interested in. Welcome to the world of Programmatic Advertising!

The Trade Desk is essentially a programmatic advertising company which operates a cloud-based platform that lets companies streamline their efforts to the apt consumer’s groups they are targeting.

This, in turn, cuts down the advertising expenditure of the company and allows it to achieve a greater ROI with its adverts.

TTD allows its customers to buy targeted ad space on many different channels like social media, video/streaming, audio and many more.

The Trade Desk’s Growth Potential

Jeff Green, chief executive officer and founder of The Trade Desk, sees China as an untapped market.

This strategic move was solidified with its launch in China earlier this year, inking deals with tech powerhouses such as Alibaba, Baidu and Tencent.

Thus far, companies such as Sheraton Hotels have successfully utilized the platform to expand their customer base greatly through its targeted advertisements.

In the next five years, CEO Jeff Green claims that The Trade Desk plans to turn China into one of its top three markets.

The company says international revenue currently accounts for about 15% in revenue but expects it to grow to roughly two-thirds of its total revenue as the programmatic industry matures.

For investors, this means that there is still huge untapped potential for The Trade Desk to grow as it would take awhile for one to see material contributions from the China market to its top & bottom lines.

With the company already growing at such a blistering pace Y-O-Y without tapping on China, one would potentially expect their growth to sustain or even increase in the future.

With earnings growth, this would inevitably lead to greater appreciation in stock prices, thus allowing the investor to potentially attain a multi-bagger.

#2 – Shopify (NYSE:SHOP)

| Market Cap. | $37.38B |

| Debt-to-Equity Ratio | 5.3 |

| Stable Top & Bottom Line Y-O-Y | Yes |

As seen in the graph, Shopify’s earnings have been growing year-on-year from 2015 to 2018. Earnings grew from $380M in 2017 to $596M in 2018, displaying a huge 56.8% growth versus the prior year.

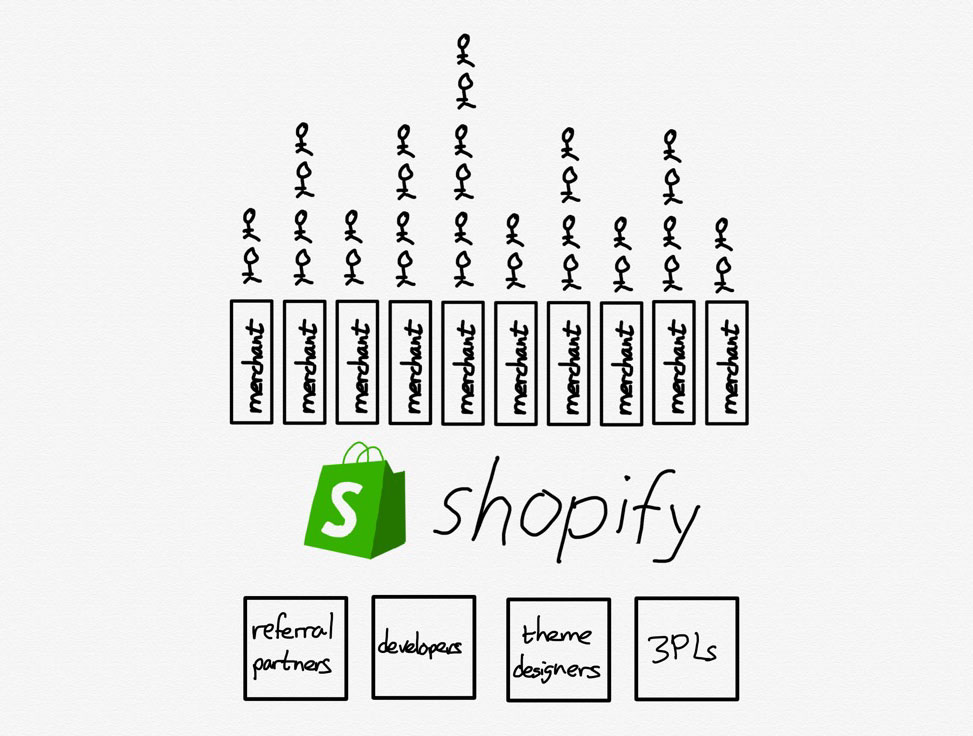

Shopify has secured its status as the e-commerce platform of choice for small entrepreneurs. Its client base and gross merchandise volume are both growing explosively.

As of June 2019, there are 820,000 Merchants from Shopify growing 55% from the prior year.

What does Shopify do?

Shopify is an e-commerce platform that allows merchants of all sizes to “set up” their own stores online. They all provide a suite of advantages such as fulfilment, payment and shipping services.

Shopify’s winning formula includes its platform’s ability to give online merchants an easy way to handle many aspects of their business: inventory management, fulfilling orders, processing payments, and communicating with current and prospective customers alike.

It is also extremely flexible with its ability to be connected with sites such as Ebay and social media such as Instagram. Small and medium-sized businesses still make up the core of Shopify’s clientele.

However, the company also offers a $2,000 a month Shopify Plus package for bigger businesses which the likes of Nestle and Red Bull utilize.

Shopify’s Growth Potential

The company estimates that there are 46 million small and mid-sized businesses around the world, and it’s only serving 1.3% of them. That leaves plenty of opportunities for Shopify to keep growing well into the future.

With the advent of the switch from traditional/physical shopping to online commerce, Shopify’s addressable market continues to grow as e-commerce captures a larger share of overall shopping.

Furthermore, one should note that Shopify isn’t a competitor to Amazon.

Amazon is an aggregator who internalises suppliers (people think they buy from amazon but actually make purchases from other suppliers).

Shopify as a platform externalises suppliers (people buy from various brands without knowing shopify powers them). There is nothing to purchase on Shopify.com other than its suite of platforms, unlike Amazon.

TLDR, Amazon is pursuing customers and bringing suppliers and merchants onto its platform on its own terms. Shopify is giving merchants an opportunity to differentiate themselves while bearing no risk if they fail.

The only way to beat an aggregator is to be a platform that externalise suppliers with differentiation.

For investors, this is a great business model which is still helmed by its charismatic and visionary founder, Tobi Lutke. In the long run, Shopify could potentially continue dominating the market and growing at a blistering pace.

With a huge untapped addressable consumer market and large growth capacities, Shopify as a fast grower could turn into one of the legendary Lynch Multi-Baggers.

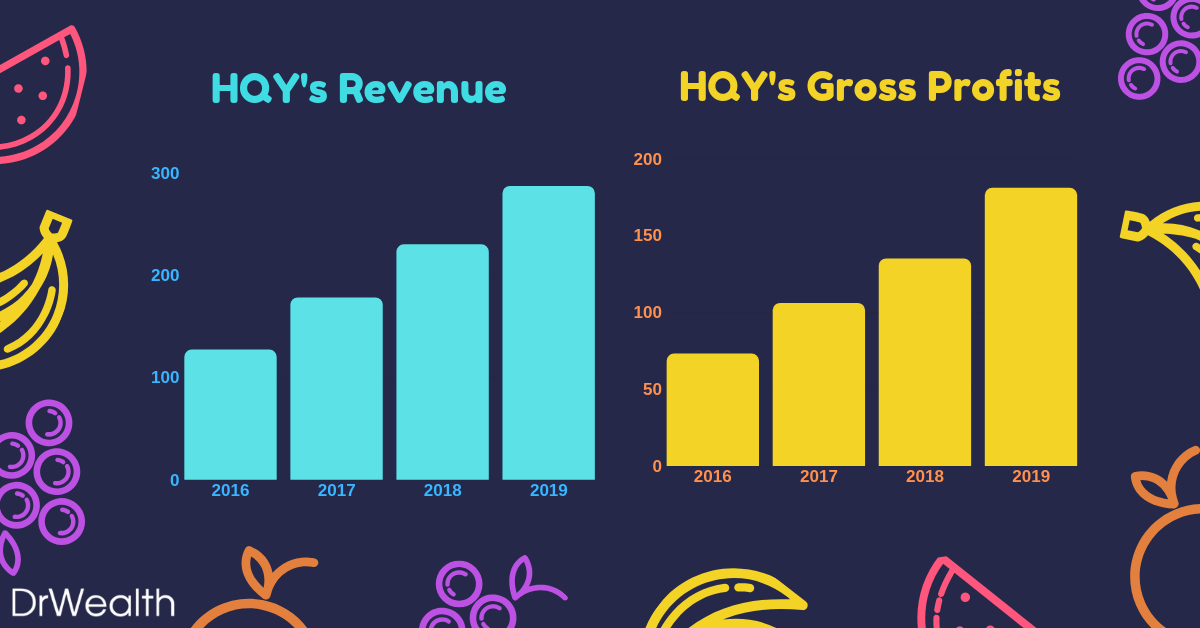

#3 – Health Equity (NYSE:HQY)

| Market Cap. | $4.95B |

| Debt-to-Equity Ratio | 7.56 |

| Stable Top & Bottom Line Y-O-Y | Yes |

As seen in the graph, Health Equity’s earnings have been growing year-on-year from 2016 to 2019. Earnings grew from $135M in 2018 to $181M in 2019, displaying a 34% growth versus the prior year.

HealthEquity is not only profitable but has also seen impressive profit growth to go with rising sales in recent years.It’s identified multiple pathways toward future expansion that includes both organic growth and potential strategic transactions.

What does Health Equity do?

Health Equity is a cloud-based platform that provides access to Health Savings Accounts (HSAs) and other health-care benefits.

HSAs were implemented by the US Federal Government in 2003. It allows one to set aside cash for certain healthcare expenses that are not covered by their insurance.

HSAs come with huge tax benefits: money placed inside of HSAs are tax-deductible, and investments inside the HSA grow on a tax-deferred basis.

Additionally, withdrawals from HSAs aren’t taxed as long as the money is used to cover qualified healthcare expenses.

They help employers and employees alike to save on healthcare costs while taking advantage of tax incentives provided.

Health Equity’s growth potential

Health Equity’s business model is also simple:

- It charges employers and health plans that are placed on the platform monthly service fees in order to provide its platform to employees and subscribers.

- It earns custodial revenue by keeping custody of customer assets such as cash.

- HealthEquity offers a payment network that allows users to have medical expenses paid directly from their HSAs, and the company collects interchange fees when those transactions go through.

With recurring revenue and simple services, Health Equity is definitely in it for the long run.

Furthermore, its founder, Stephen Neeleman was one of the doctors that lobbied for the federal government to implement HSAs and then subsequently built the platform, Health Equity to trade the accounts.

Rising Health Care costs will definitely be a huge proponent that drives up the demand for Health Equity services and products.

As the number of discerning healthcare consumers expands exponentially, interest in Health Savings accounts and highly deductible savings plans will rise in tandem.

For investors, the rising number of consumers being aware of Health Savings Accounts will drive demand for Health Equity’s platform. This would subsequently propel top-line sales and in turn, earnings.

With Earnings growth comes appreciation in stock prices.

Summary of Fast Growers stocks

So there you have it. The Fast Growers Category explained in accordance with Peter Lynch’s guidebook. If you choose wisely, this is the land of the 10-40 baggers and even the 200 baggers. However, Lynch reminds us that there’s plenty of risk in fast growers, especially in the younger companies that tend to be overzealous and underfinanced.

The stock market also does not look too kindly fast growers that run out of steam and turn in to slow growers. Hence, it is essential to figure out when the company is going to stop growing (lack of future plans, depreciating financials and loss of key leadership).

As one would notice, Peter Lynch identifies a stock using Qualitative Analysis before diving into the Quantitative.

That means he looks at a stock’s story before he looks at a stock’s business. There is nothing inherently wrong with that.

Whether you approach it from the numbers angle or the story, both ways work. However, we would advise retail investors to focus on approaching stock investing from the quantitative side of things.

This is to avoid biases and to avoid falling in love with a stock’s story. To hunt growth stocks, we have developed a robust, evidence-based framework that has delivered stellar returns per year historically. You can join us at a live session to learn more.

Next, we would be going in-depth into one of the six different categories pointed out by Lynch – The Asset Plays

Peter Lynch Stock Category 3: Asset Plays

Asset Plays are stocks that are believed by investors to be undervalued because the current price does not reflect the current value of the company’s assets displayed on its balance sheet.

The rationale for purchasing the stock is that the company’s assets are being offered to the market relatively cheaply, making it attractive to investors.

It would be sort of like buying a house for $0.40 on the $1.

Investors who utilize this strategy believe that the market overreacts, resulting in stock price movements that do not correspond with a company’s long-term fundamentals, giving an opportunity to profit when the price is deflated.

In fact, here at Dr Wealth, we employ our Conservative Net Asset Valuation (CNAV) method to identify to evaluate and select deeply undervalued Asset Plays.

We provide “Skin in the Game” case studies of our winning stocks that were hand-picked using our proprietary CNAV screener, substantiating them with past transaction statements.

We would thus be picking stocks utilizing the following criteria to select our Top 3 Asset Plays:

- Company’s CNAV2 value is at a discount from Market Price.

- Company’s POF score is 2 and above.

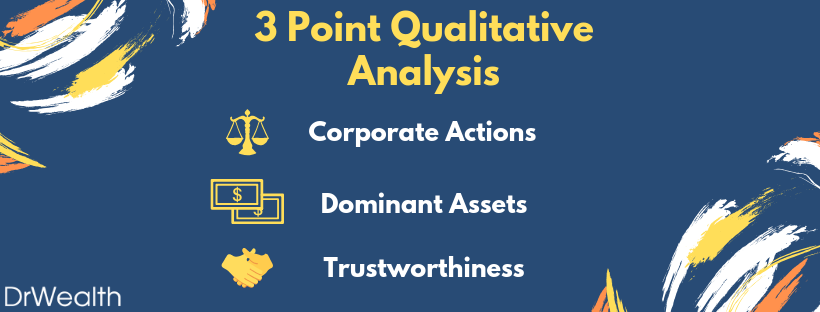

- Passes our 3 Point Qualitative Analysis

To elaborate a little further on the above criteria:

- Company’s CNAV2 value is at a discount from Market Price

This is the formula we use to calculate a stock’s Conservative Net Asset Value:

- Good Assets are defined as Cash, Cash Equivalents, Lands and Buildings.

- IGA are Receivables, Investments, Inventories, Intangible Assets.

All of which can be found in the Balance Sheet of the company’s financial statements.

We would then take the CNAV2 value, divided by total shares outstanding to find the CNAV2 per-share value.

Thus, if the CNAV2 per-share value is HIGHER than that of the current price per share, it is deemed to be on a discount.

- Company’s POF score is 2 and above.

To make our selection more stringent, we turn to Dr Joseph Piotroski’s F-score to find fundamentally strong low price-to-book stocks that are worth investing in.

As we have already added conservativeness, we do not need to adopt the full 9-point F-score. A proxy 3-point system known as POF score would be used instead.

It stands for Profitability, Operating Efficiency and Financial Position.

- For Profitability: Price to Earnings Ratio = 0 < PE < 15

- For Operating Efficiency: 2 out of 3 years with positive cash flow from operation

- For Financial Position: Debt to Equity Ratio < 100%

The stocks selected has to have a POF score of 2 and above.

To learn more about the POF score and how we use it in our investment strategies, click here.

- Passes our 3 point Qualitative Analysis.

- Corporate Actions:

- Since an Annual Report is merely a “snapshot” of the company’s financials, things can change rapidly. Thus, we have to look out for corporate actions that the company will have to disclose under the Singapore Exchange. For example, share buybacks, share splits, disposal of assets, etc.

- Dominant Assets:

- When you look at the company’s financial statements, you must assess it for the assets you are purchasing. We also want to watch out for assets that might be depreciating very quickly such as food produce and or inventories that might be outdated by industry standards.

- Trustworthiness:

- Did the company financially engineer its books? Is management open and honest? Can they be relied upon to not “cook” their books?

An easy way to bypass such subjective questions is to look at whether management owns the majority of the shares in the company.

Today, we would be looking at the Hong Kong Stock Exchange market due to the recent correction caused by the protests. This resulted in many counters being ‘On-Sale’ even though its fundamentals have not faced any drastic changes.

Why these 3 stocks?

To facilitate your reading, we have structured the content into clear and concise points to sum up what you have to know:

- What does the company do?

- What are their assets?

- Why is the stock undervalued?

While there isn’t a hard and fast exit strategy, at Dr Wealth we would either sell at the 3 year holding period, when the Financial Fundamentals change or when a key qualitative point has been changed (i.e. change of CEO/founder steps down).

- 3-year holding period: We wouldn’t want to be stuck in a value-trap for years and would rather re-allocate our capital to more promising counters we identified.

- Financial Fundamentals change: This is mainly signalled by a change in the POF score of a company. If the score drops below its prior number, it should be a good reason to review one’s decision.

- Key qualitative point has been changed: Imagine Amazon without Jeff Bezos or Facebook without Mark Zuckerberg. There would be huge distress should the company fail to find a suitable replacement for the leadership. However, it is not all doom and gloom, evident in Tim Cook’s helming of Apple after Steve Jobs.

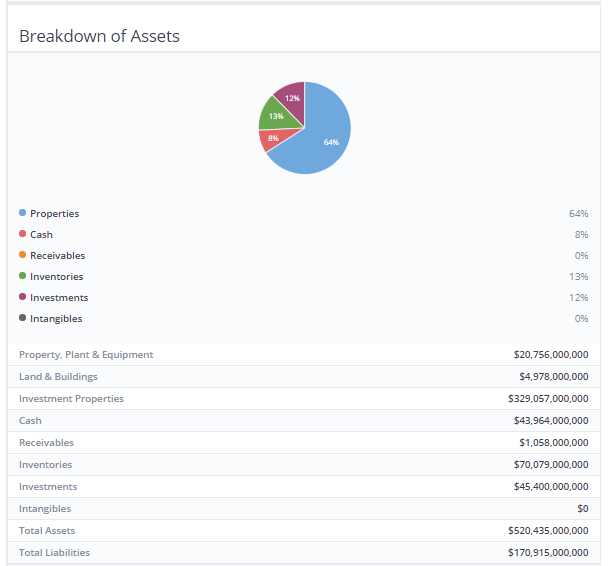

#1 – Emperor Watch & Jewellery (HKSE:0887)

| Market Cap. | $1.173B |

| Market Price | $0.173HKD |

| CNAV2 Value per share | $0.386HKD |

| Net Asset Value per share | $0.659HKD |

| POF score | 3 |

| Potential Profit | 281% |

What does the Company do?

Emperor Watch & Jewellery is a retailer of European-made internationally renowned watches such as Patek Philippe, Rolex and Tudor. This is coupled with the sales of self-designed fine jewellery under its own brand, ‘Emperor Jewellery’.

The company has a history of over 75 years, establishing over 90 stores across Hong Kong, Macau, mainland China, Singapore and Malaysia, as well as an online shopping platform, and now has over 1,100 staff.

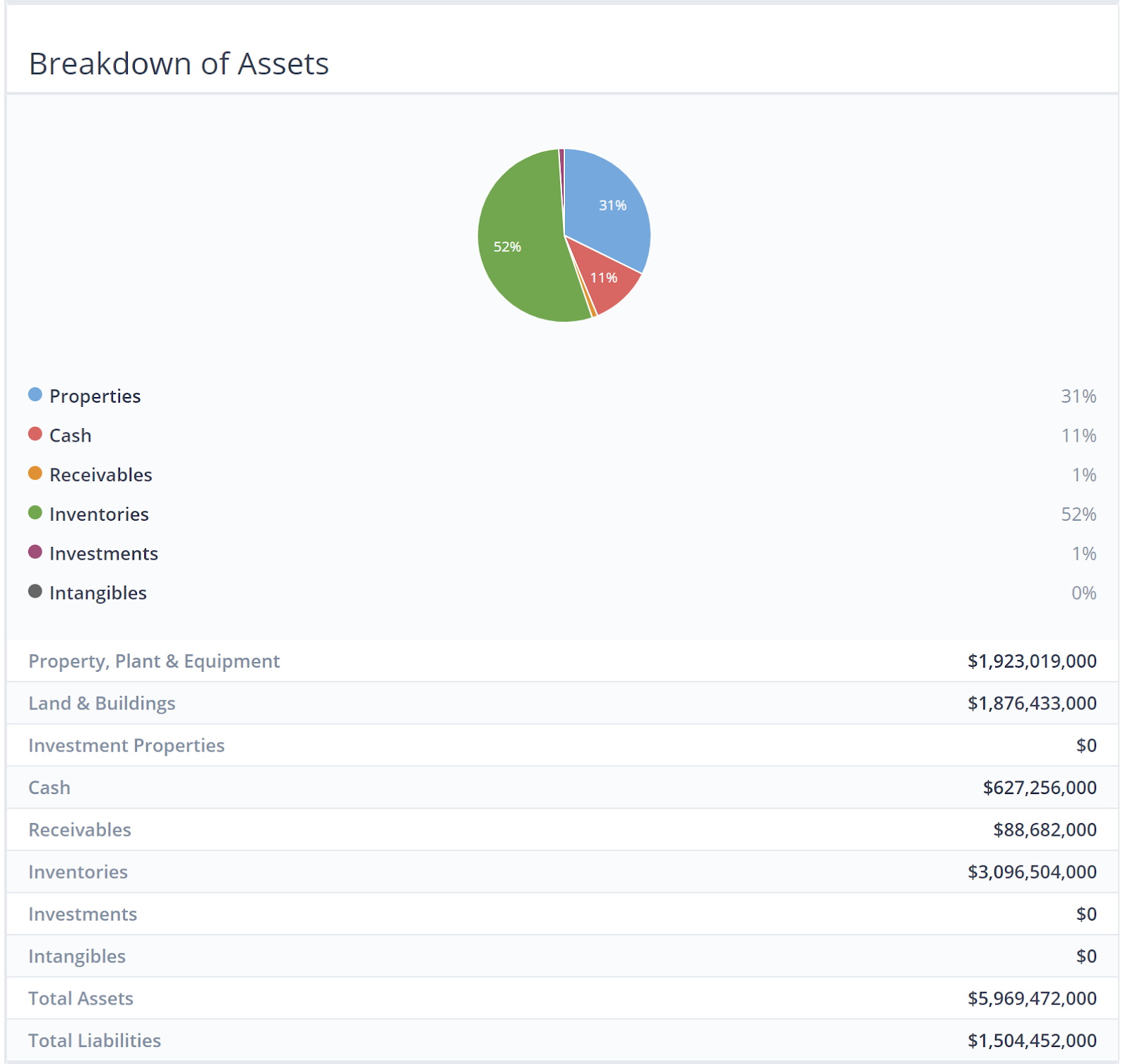

What Are Their Assets?

As seen in the infographic above, Inventories and Properties make up the bulk of their assets. There is a whopping HK$3.09 billion worth of luxury watches and Jewellery.

My hypothesis was that it wouldn’t be that bad because luxury watches and jewellery retain value pretty well as long as they are not worn and still in good condition.

We went ahead to discount the current inventory of watches and jewellery at 50%. We should account for a large margin of safety when calculating the valuation of Emperor Watch & Jewellery.

Why is the Stock Undervalued?

The Company’s core strategy focuses on maintaining its position as the leading watch and jewellery retailing group in Greater China, coupled with an eye on expansion beyond the region.

As most of their customers are mainlanders, boutique stores that peddled luxury goods such as watches and jewellery enjoyed the patronage of this swell of new customers as a result.

However, most of this all came to a halt when President Xi Jing Ping decided to rein in on the corruption.

This discouraged ostentatious displays of wealth in public. Sales of luxury goods to Chinese consumers slowed for a time and as earnings dropped, so did share prices.

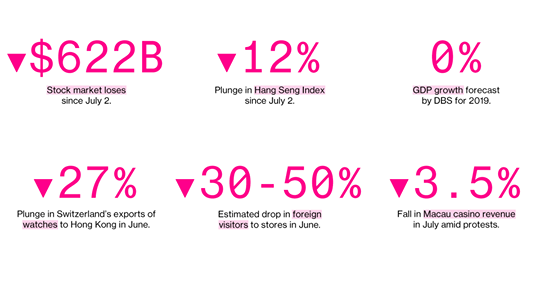

Coupled with the recent 10 straight weeks of anti-government protests in Hong Kong, stock prices in the HK Exchange have inevitably taken a massive beating. This is without even mentioning the massive backdrop created by the Trump-China trade war affecting prices as well!

More than $600 billion of stock market value has been erased since early July thanks to the riots and protests.

The culmination of all these events have thus done something favourable for us; create opportunities for us to businesses at fantastic bargain prices.

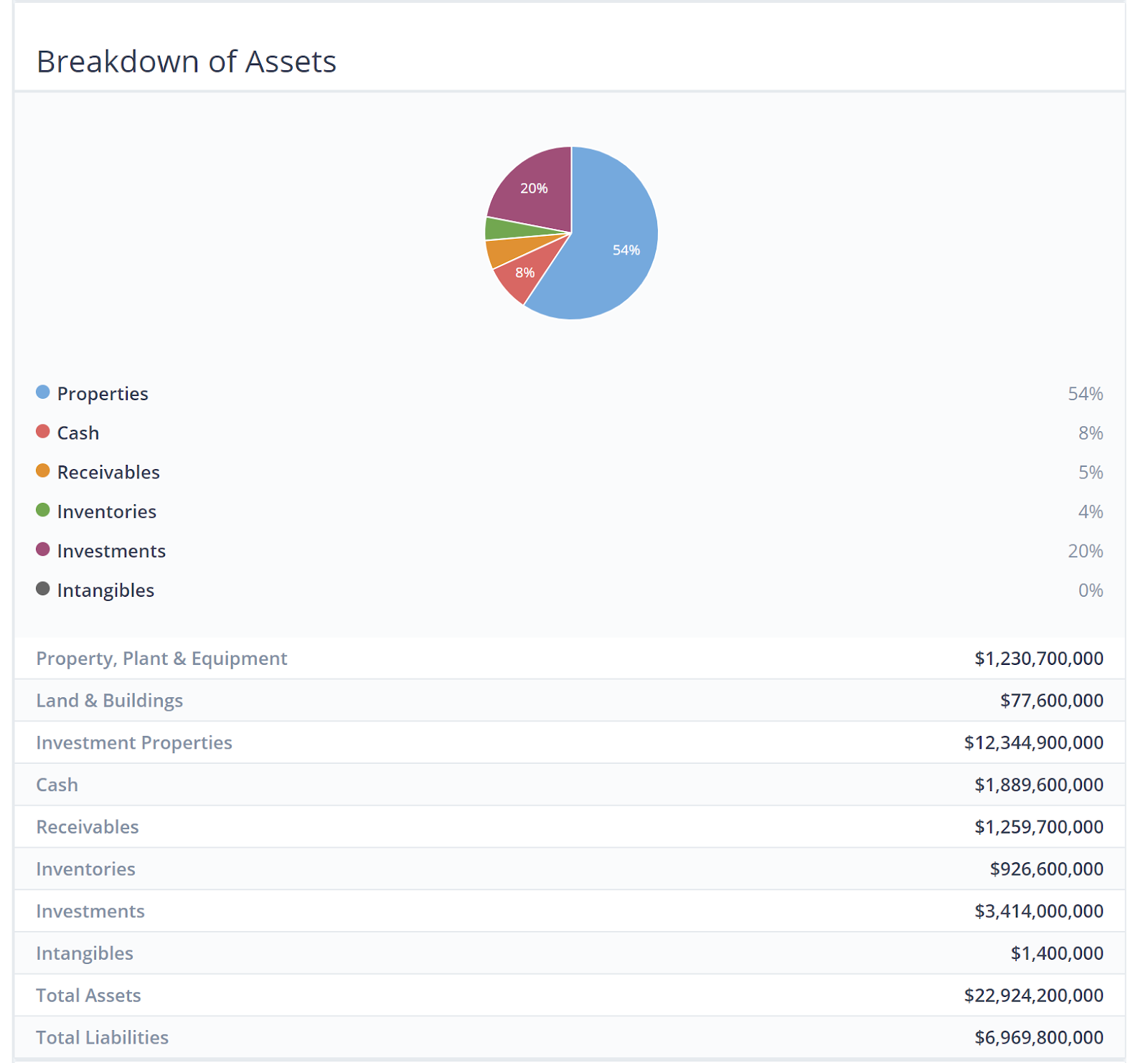

#2 – Wheelock Co. & Ltd. (HKSE:0020)

| Market Cap. | $97.101B |

| Market Price | $47.4HKD |

| CNAV2 Value per share | $68.357HKD |

| Net Asset Value per share | $105.846HKD |

| POF score | 3 |

| Potential Profit | 121% |

What does the company do?

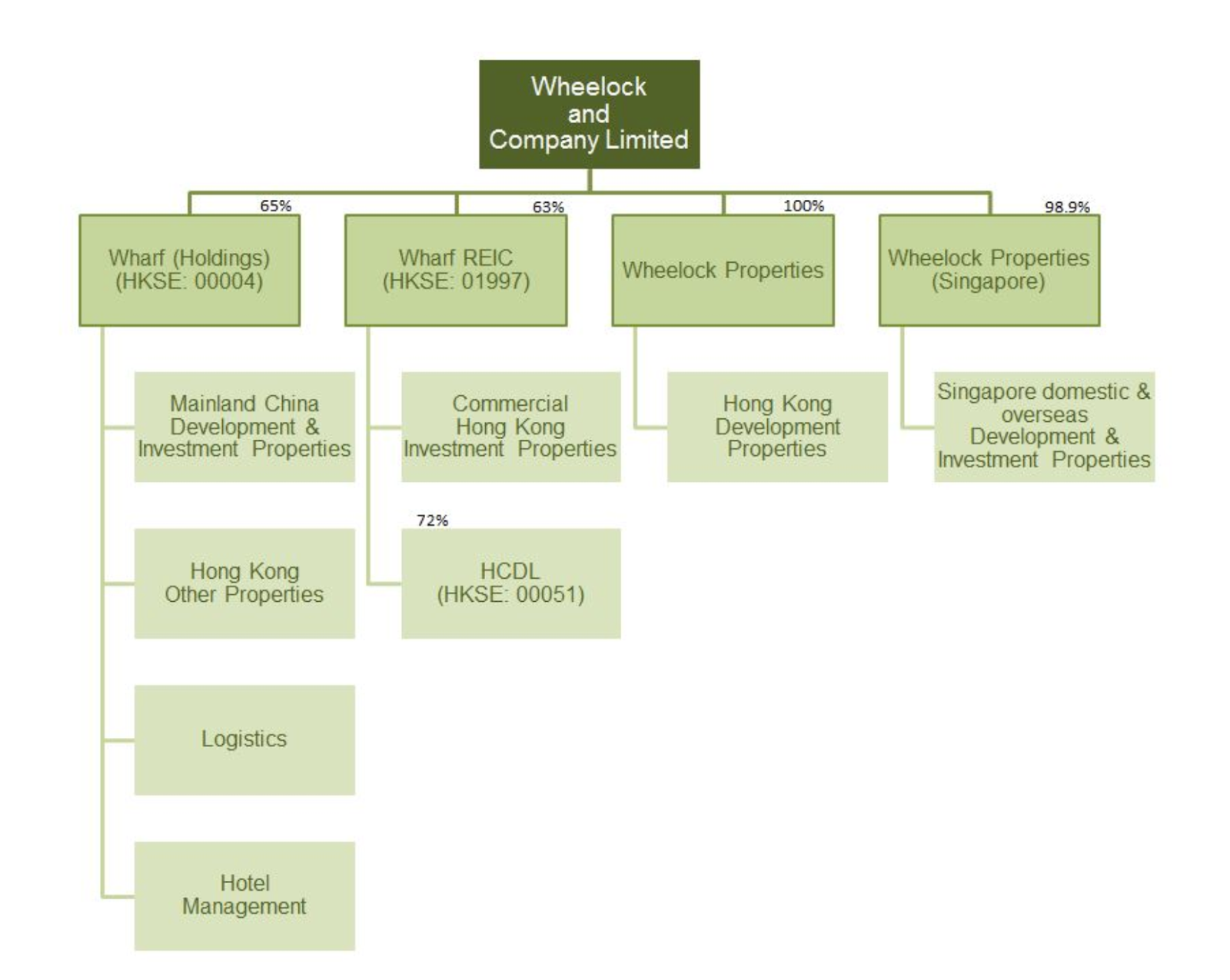

Wheelock & Co. is principally engaged in property development in Hong Kong, and in property investment and development in Singapore.

Their major subsidiaries include Wharf (Holdings) Limited (HKSE: 00004), Wharf REIC Limited (HKSE: 01997), Wheelock Properties Limited and Wheelock Properties (Singapore) Limited.

- Wharf (Holdings) (HKSE: 00004) 65%-owned by Wheelock, is a listed company principally engaged in property development and investment in Mainland China, other Hong Kong properties as well as non-property business in Hong Kong and the Mainland.

- Wharf REIC (HKSE: 01997) 63%-owned by Wheelock, is a listed company which owns and operates premium, quality investment properties in prime locations in Hong Kong, as well as certain Mainland China property interest.

- Wheelock Properties 100%-owned by Wheelock, spearheads the Group’s property development business in Hong Kong.

- Wheelock Properties (Singapore) 98.9%-owned by Wheelock, is the Group’s property arm in Singapore, where it focuses on luxury residences and retail leasing.

What are their Assets?

As seen in the infographic above, Properties make up the bulk of their assets. This should be rightfully so as they are engaged in the property development business.

Due to the sheer amount of properties available in the company, we would only touch on the assets of Wheelock Properties here.

Kindly refer to the company’s website should you like to find out more about its other major subsidiaries asset breakdown.

Why is the stock undervalued ?

- This was mainly caused by the China-Us trade tensions which were exacerbated in April due to President Donald Trump’s legendary tweet, stocks listed in the HKSE took one of the biggest hits and remained under pressure.

- Bullish sentiment on Chinese/Hong Kong stocks quickly faded as Trump unexpectedly announced he would more than double the levies on US$200 billion worth of Chinese imports and threatened to include more items that are not covered by tariffs. This thus caused Wheelock’s stock to correct due to macro pressures.

- The next correction was due to the anti-extradition bill protests in Hong Kong. This was the second macro headwind that caused the Hong Kong Stock market to plunge, taking Wheelock’s share price with it.

#3 – HKC (holdings) Properties (HKSE:0190)

| Market Cap. | $2.48B |

| Market Price | $4.69HKD |

| CNAV2 Value per share | $15.067HKD |

| Net Asset Value per share | $24.966HKD |

| POF score | 3 |

| Potential Profit | 420% |

What does the company do?

The Group is a Hong Kong-based property developer focusing on investing and developing property projects in Mainland China and aims to develop high-quality products to create sustainable value for its shareholders.

The Group has a diversified property portfolio model with investments in both residential projects for sale and commercial projects mainly for rental income.

The group is organized into 3 main operating segments:

- Commercial Projects – This segment is in the business of the development of commercial properties mainly for rental income.

- Residential Projects – This segment is in the business of the development of Residential properties mainly for sale.

- Renewable Energy Projects– This segment is in the business of the private development of wind farms.

Over the long term, the Group seeks to maintain a balance between residential development for sale and commercial investment properties for lease in order to create a sustainable model with growth potential.

Residential properties for sale generate fast turnover, which should enhance return on equity. Investment properties for lease, on the other hand, create steady recurring income and cash flow as well as long term capital appreciation and are relatively immune from the periodic restrictions on residential properties.

The Group has also made an investment in the renewable energy sector and believes shareholders may benefit from China’s need to develop non-polluting sources of energy.

What are their Assets?

As seen in the infographic above, similar to Wheelock & Co, Properties make up the bulk of their assets. This should be rightfully so once again as they are engaged in the property development business.

The assets are mostly located around the more developed, coastal regions of China – where population density and income levels are much higher.

Why is the stock undervalued?

This could largely be attributed to the slowdown of the Chinese property sector in 2018. China’s massive property market is expected to cool further in 2019, with smaller price rises and falling home sales adding to pressure on the world’s second-largest economy, a Reuters poll showed.

As a result, residential sales volume began declining in the second half of 2018, with declines of 1% year on year in September and October and 4% in November. It increased by 2.5% in December, but poor Chinese New Year’s data suggest that the decline will continue into 2019.

Moreover, the price rise growth for new residential properties has decelerated for the third straight month. In January, residential prices for 70 major cities increased by only 0.61% compared to December, the slowest pace in nine months.

Nice interpretation of the book. I gained new insights after reading your article too. Thank you