Buying a house is one of the biggest financial decisions that one has to make. No one would want to lose money from a property they bought. If one has the luxury to wait, Singaporeans would usually prefer Built-to-Order (BTO) flats to a resale flat because of the heavily subsidised by the government.

An example is the May 2021 BTO launch in Macpherson, you can see that prices are generally 20% lower as compared to resale flats within the same vicinity:

However, with the introduction of the Prime Location Housing (PLH) model, is it still worth it to buying BTOs in prime locations?

What is the Prime Location Housing (PLH) model?

The Prime Location Housing (PLH) model was first introduced on 26 October 2021. It aims to keep prime HDB flats in the central and greater southern waterfront areas affordable and inclusive.

The first Build-to Order (BTO) project under this model will be located in Rochor which will be launched this November. You can check HDB’s website for more updates on the upcoming BTO sales launch. Do take note that the PLH model will not affect the houses that were previously built in prime locations.

Flats that are under PLH model will be subjected to the following:

- 10 years minimum occupation period (MOP)

The minimum occupation period (MOP) is the period of time that you are required to physically occupy your flat before selling it on the open market. It is calculated from the date of the key collection and a typical BTO flats have a 5 years MOP.

However, if you were to buy the flat under the PLH model, it will be double the usual period.

- 6% subsidy will be clawed back upon resale

When selling their subsidised house on the open market for the first time, flat owners would have to pay the government a percentage of the resale amount.

Under the PLH scheme, flat owners would have to pay 6% of the resale price or the flat’s valuation, whichever is higher to HDB when they sell their homes, on top of the usual resale levy. This is to cover HDB’s subsidies on BTOs in prime locations, which helps to keep these houses affordable.

However, the good news is that the 6% will not be applied to subsequent resale transactions.

- No renting out the whole flats

Flats owners under the PLH scheme would not be able to rent out the whole flat, even after the MOP is over. If you’re thinking about locking a room up and renting the rest without physically staying in, it is not allowed either.

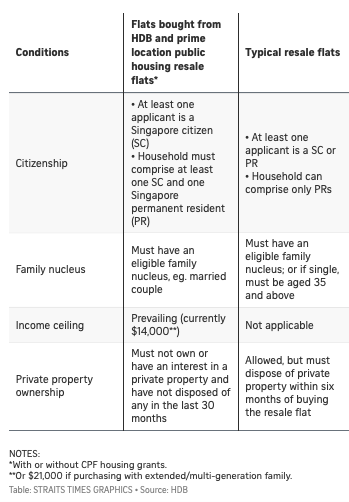

- Stricter eligibility criteria for buyer such as family nucleus and income ceiling

Even if the house is put up in the open market, future buyers would have to follow the same prevailing eligibility conditions as with buying the flat directly from the HDB.

This might limit the size of the resale market after MOP.

- Reduced number of flats set aside for Married Child Priority Scheme (MCPS)

Married Child Priority Scheme (MCPS) is a scheme that helps a married couple child and parents to live with or close to each other. If the parents and married child stay within 4km, they will be entitled to this scheme.

With the new PLH model, there will be a reduced number of flats set aside for certain projects in prime locations. For the upcoming Rochor BTO, MCPS flats are reduced to two thirds of the usual quotas.

What is the potential capital gain from the Rochor BTO?

Based on the flat prices provided from the HDB, the houses at Rochor will cost a maximum of $770,000 for a 4 room house.

Due to the prevailing eligibility of the household income ceiling of $14,000, the maximum bank loan you are looking at would be about $838,953.

This means that the potential flats under PLH model will only go up to a maximum of $1.1million in a resale market.

Assuming that you buy the most expensive unit at the Rochor BTO for S$770,000 and are subsequently able to sell it at $1.1 million, your total capital gain will be $330,000 (excluding the 6% clawback and charges).

Even with the additional 6% clawback, you would still be able to enjoy at least $264,000 capital gains within the next 17 years in 2038. This is due to the fact that flats owners of Rochor BTO will have to wait for 71 months before the house completion (the estimated completion date is 2Q2028).

So, does it still make sense to buy the Rochor BTO?

The HDB resale flat prices have risen across the board. Looking at the resale prices in the Central area, it has increased by 3.47% for 3-room and 4-room flats.

However this slow rate of increase is due to the older flats. If you were to compare with those prime flats like SkyTerrance @ Dawson (Queentown), which entered the resale market 2 years ago, you’re looking at a price increase of 17.54% till date.

However, with the new PLH model, the house price might end up rising to a maximum of $1.1 millions even with a healthy appreciation potential. Therefore, to answer whether it is worth buying the Rochor BTO, it is important to know your objectives and if you are willing to wait for 17 years before upgrading to a new house.

My Thoughts

If you are choosing the house for your own stay, this BTO will definitely win you over because of its location and accessibility. However, couples or families might have to rethink about their own family planning as the extended 10 years MOP might be a problem in future.

If you’re considering the BTO as a property investment, this might not be an ideal place for you due to the limitations imposed by the PLH scheme. You might want to consider an Executive Condominium or private properties which could deliver higher appreciation rates compared to BTO/HDB flats.

Here’s a comparison between BTO vs Executive Condominium if you would like to dive deeper. And if you’re looking for a proven property investing strategy, read about the BRRRR strategy here.