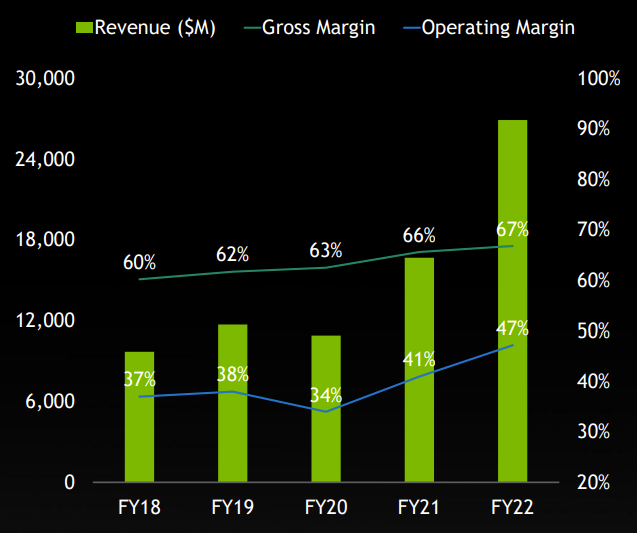

NVIDIA (NASDAQ:NVDA) is a well-liked growth stock, particularly from a fundamental standpoint. The company’s share price increased 120% in 2021 after having a phenomenal year, with revenue rising by 61% year on year and gross margin inching ever higher.

However, with a new marco environment in 2022, we are seeing the reverse reaction. NVIDIA has returned nearly all of its 2021 gains amidst a 50% drop.

What is the cause of this stock’s rise and fall? Should investors start considering investing in NVIDIA?

What does NVIDIA do?

For those who are unfamiliar, NVIDIA is the market leader in discrete graphics processing units (GPUs). In simpler terms, it is a type of chip that allows for graphics rendering as well as the processing of large amounts of data at a faster rate than Central Processing Units (CPUs).

Gaming, artificial intelligence, autonomous vehicles, cryptocurrency mining, robotics, augmented and virtual reality are just a few applications that rely heavily on GPUs.

Many of these applications are in fact , experiencing rapid growth. In gaming, the growing number of live streamers, broadcasters, artists, creators, and eSports games, have enlarged the demand for NVIDIA gaming GPUs. GPUs are also widely utilized in research, from simulating molecular dynamics to climate predictions.

You may have landed on this article due to search recommendations from cloud service companies such as Google, which rely on GPUs to churn out the best recommendations. GPUs are also utilized in social networking, online shopping, live video, translation, AI assistants, navigation, cloud computing, fraud detection, autonomous driving, medical imaging, and various other applications.

How Nvidia makes money: segment breakdown

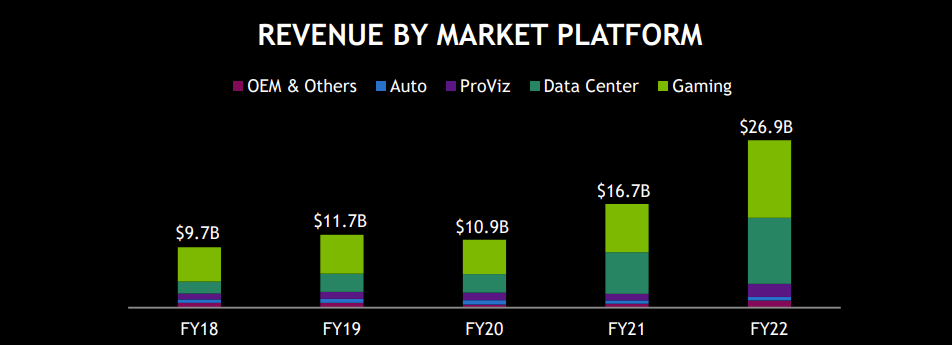

Overall, NVIDIA platforms address four markets: gaming, data centre, professional visualization, and automotive, with the first two being the primary drivers for the company, accounting for 46% and 40% of its FY2022 revenue, respectively.

A brief description of the value created by NVIDIA in various segments

- Gaming: Improves gaming experience by providing smoother, higher-quality graphics.

- Data Centre: Accelerating the most compute-intensive workloads, such as AI, data analytics, graphics, and scientific computing. On the whole, it improves the performance and energy efficiency of high-performance computers and data centers.

- Professional Visualization: Improves the capabilities of various visualization technologies such as computer-aided design (CAD), medical instrumentation, video editing, and special effects for films, among others. All of which require a significant amount of computational power to render.

- Automotive: Provide an end-to-end solution for achieving an AI that can drive the car in completely autonomous mode.

High Competition in GPU market

Another aspect of this industry is competition. It is hardly surprising that NVIDIA operates in a very competitive market, given its highly lucrative business. There is no monopoly, and with rapid technological breakthroughs, NVIDIA might easily be pushed aside if they do not continuously improve. Taking Intel, which formerly dominated its competitor but has now fallen behind due to minor missteps.

Let us now look at NVIDIA’s competitors. NVIDIA’s direct competitors, which design discrete and integrated GPUs, custom chips, and other accelerated computing solutions, include Intel and AMD, both of which are attempting to produce better-performing chips of their own.

Indirectly, large internet service providers like Alibaba Group, Alphabet, and Amazon have internal teams building chips that contain accelerated computing functions as part of their internal solutions or platforms.

Last but not least, new competitors or combinations of competitors may develop and gain significant market share moving forward.

Nvidia’s Financial Performance

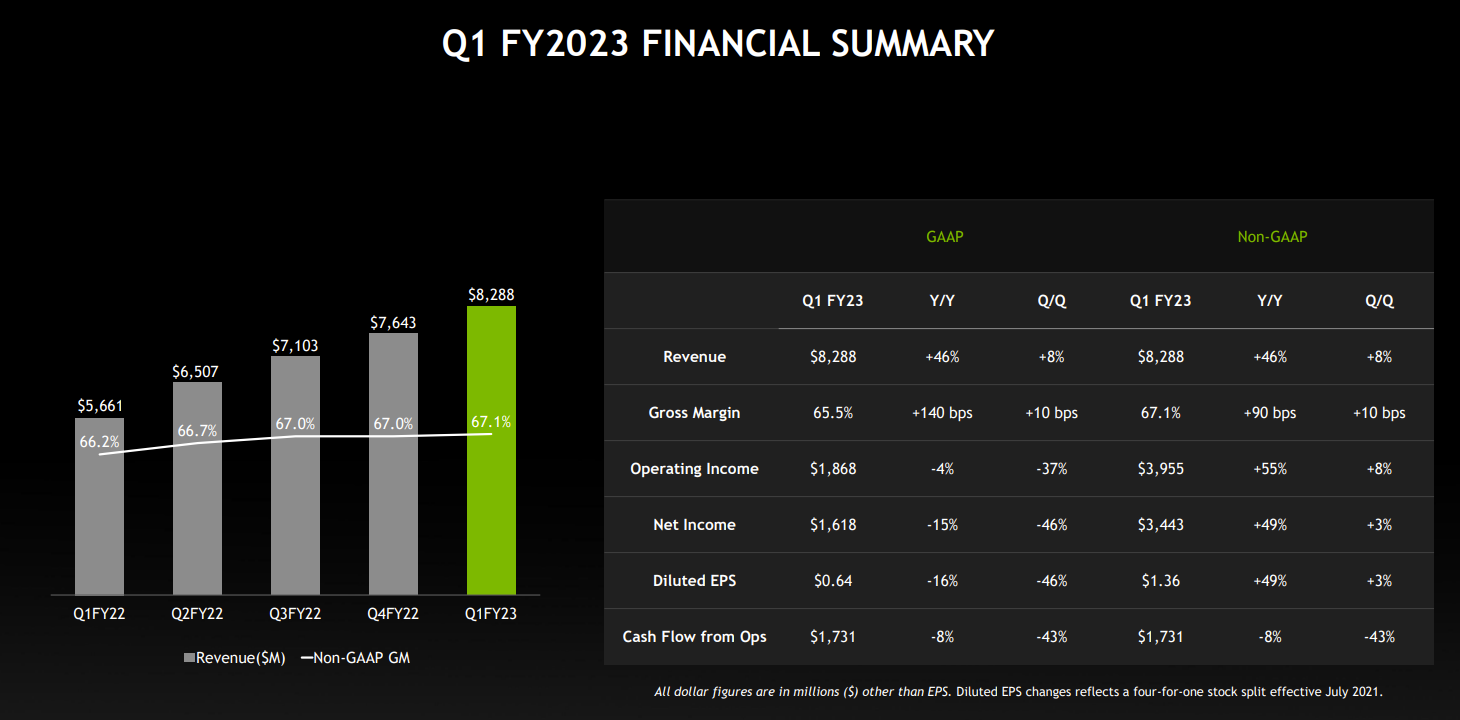

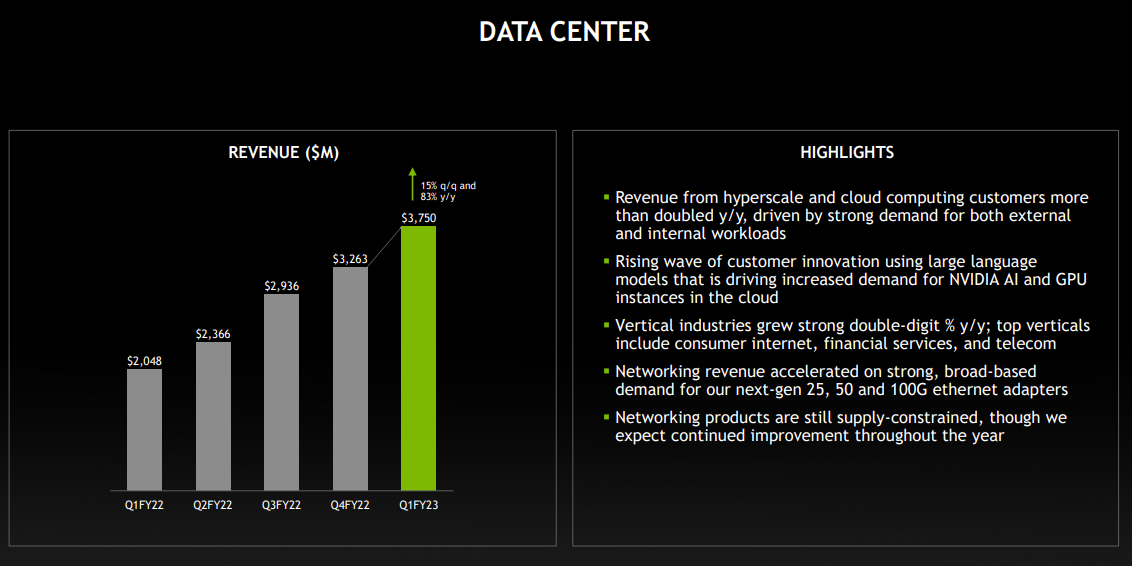

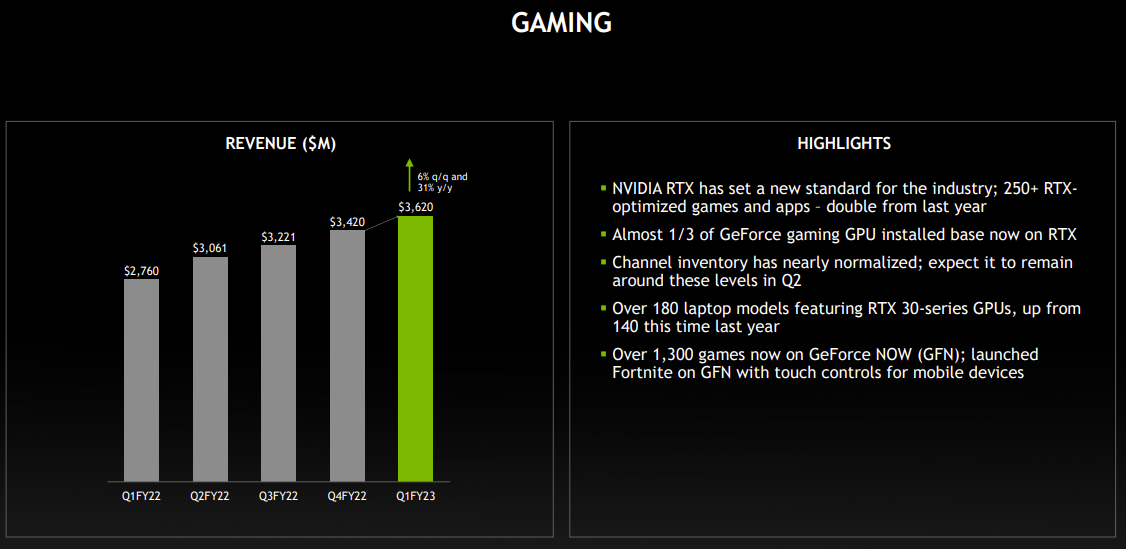

Moving on, NVIDIA revenue has been consistently growing for the past few quarters, with its latest quarter FY2023 Q1 reporting a historical high of $8.29 billion, up 46% from a year ago and 8% from the previous quarter (Revenue from Data Center up 83% year on year and gaming was up 31% year on year). This comes as demand for cloud computing and gaming increased as we became more interconnected, in addition to the push factor of the pandemic.

Digging deeper, we can observe that the growth rate for data centres has been faster than that of gaming to the point where it has recently exceeded in terms of revenue. However, whether or not this trend will continue depends on macroeconomic variables. Rising interest rates and inflation are squeezing both corporate and consumer pockets. Add to that, cryptocurrency, which is heavily dependent on GPUs, is experiencing a new winter.

In terms of margin, as Nvidia continues to benefit from economies of scale, its margin has continuously increased. This margin has increased slightly to 67% in Q1 FY23, which is a healthy indicator.

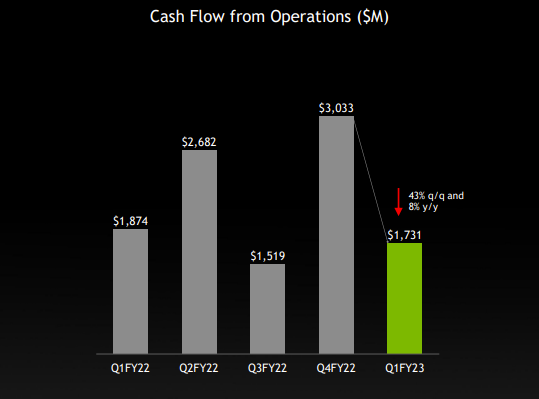

Nonetheless, while revenue increased, net income and cash flow from operations decreased significantly.

According to Nvidia, the sequential fall in cash flow from operations primarily reflects advanced payments on supply agreements, resulting in a 43% drop in cash flow from operations.

As a result of this situation, NVIDIA’s quarterly cashflow becomes erratic, making it difficult to assess its performance.

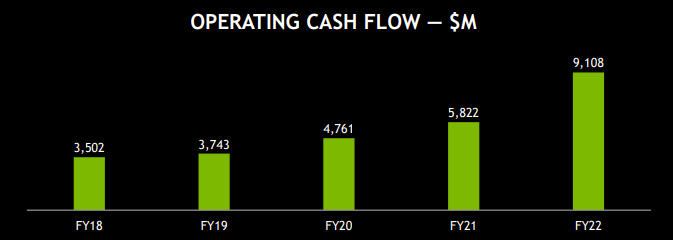

Zooming out on a year-to-year basis, we will have a better picture and can see that NVIDIA’s operating cash flow has been improving steadily over the years, which is what a fundamentally solid company should provide.

What about net profit? Earnings per share fell 46% quarter over quarter and 16% year over year. This is primarily due to the $1.35 billion acquisition termination cost with Arm, which required NVIDIA to write off the prepayment made last year. This, combined with the fact that it is a one-time expense, should not have had a significant impact on NVIDIA, so what went wrong? Why did NVIDIA decline by more than 50%?

Why Is NVIDIA stock Dropping?

There could be numerous explanations for this drop in share price, but I believe it was caused by changes in the macro variables and a poor outlook.

Unfavourable macro environment

The rising interest rate and inflationary environment haven’t been kind to NVIDIA, which is generally considered a growth company. A rising interest rate would inexorably reduce NVIDIA’s cash flow-based valuation. Aside from that, rising inflation meant potentially increased expenses. While NVIDIA might pass the cost on to its users, this could affect its customer base, causing revenue to suffer.

In addition to the slowdown in consumer spending, we are witnessing a bear market in cryptocurrency, a market that is heavily reliant on GPUs for mining.

All of this inevitably leads to the next factor, which is a worse-than-expected outlook.

‘Poor’ outlook

Looking at the two main generators, Nvidia Gaming and Data Center, both have provided a strong 5-year CAGR of 25% and 66 %, respectively. Going forward, NVIDIA will endeavour to seize this market from the growing population of gamers and creators, eSports, VR, gaming laptops, and cloud gaming, as well as the rapid usage of AI and graphics in every major industry. However, maintaining such rapid growth may prove difficult for the company.

In its recent quarter, NVIDIA has beaten its previous outlook of $8.10B (Actual revenue was $8.29B). Moving forward, it anticipates $8.10 billion in revenue or a 24.4% year-on-year increase. Of course, it’s impressive, but it represents a slowdown from the previous quarter’s 46% rise. This here, could have been the reason why NVIDIA is showing a drop.

How much is Nvidia worth now?

Even with slower growth, NVIDIA is still a wonderful firm with strong fundamentals, but is it a good time to buy now?

At present, NVIDIA’s price-to-earnings ratio is 40.7, which is still very expensive compared to the broader market S&P500, which has a PE of 19.2. Nevertheless, if we consider its recent peak was about 105 and that NVIDIA belongs to the Information Technology sector, a sector which typically trades at a higher valuation attributing to its growth, a PE of 40.7 seems reasonable now.

As a matter, NVIDIA’s current PE is the lowest since October 2019.

Source: TradingView

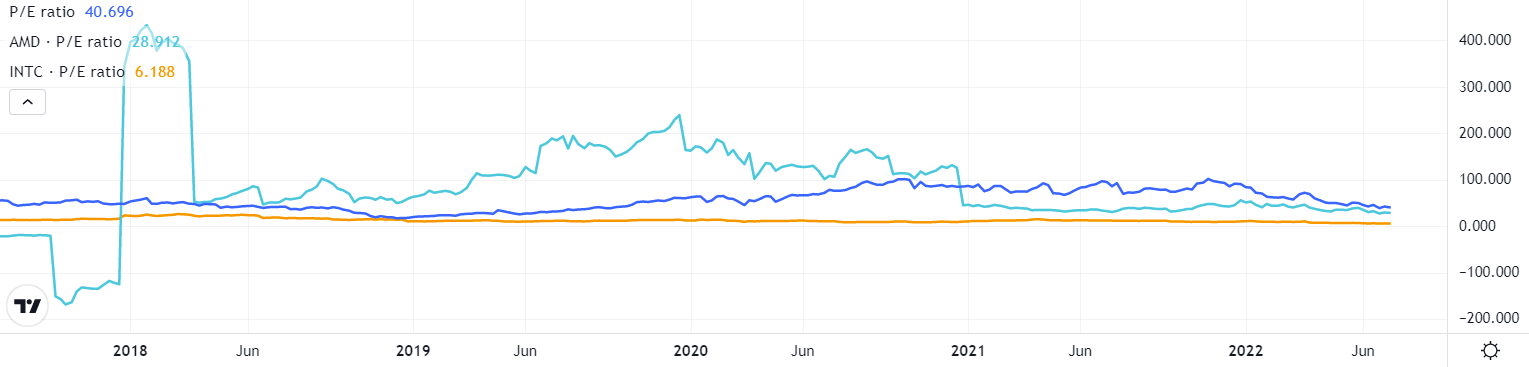

However, comparing this with its peers, we may tell another story.

Source: TradingView

Per the chart, NVIDIA (40.7) has a higher PE than AMD (28.9) and Intel (6.2). Well, Intel may not be a good comparison because it is an integrated device manufacturer that has integrated the bulk of the semiconductor manufacturing process, i.e. it designs, manufactures, tests, and packages its chips entirely in-house. NVIDIA, on the other hand, is a fabless company that just handles design while outsourcing the rest of the process to other businesses such as TSMC.

However, even after excluding Intel, NVIDIA appears to be more expensive due to its higher PE ratio. And we have not even considered the growth rate which AMD is expected to have a higher growth rate moving forward.

Ultimately, NVIDIA has solid fundamentals and ticks most of the criteria for a long-term investment. Unfortunately, the pricing may not be as appealing when compared to its peers or even the broader market, raising the question of if there are better alternatives to NVIDIA.

Conclusion

NVIDIA has seen great growth in recent quarters, with its top two revenue generators increasing by 83 % and 31 % year on year, respectively. However, given the current macro environment, these segments may experience a slowdown. Aside from management’s lower growth prediction, analysts predict slower growth (low teens) for NVIDIA. All of this has resulted in a decreased valuation for the company and, perhaps, a drop in its share price.

In terms of valuation, NVIDIA appears to be more reasonably valued now, albeit it may still be more expensive than comparable firms. Nonetheless, this is a fundamentally sound stock, and long-term investors can simply disregard the short-term volatility and focus on the long-term horizon, in which NVIDIA will play a significant role in shaping our digital world.