It is Tax Filing Season in Singapore once again. From 1 March 2024 to 15th April 2024 (or 18th April 2024 if you’re e-filing), individuals are required to file their income tax so that the taxman determines what share of your 2023 earnings it is entitled to.

For many it is a simple enough process, easily accomplished during the half time of a soccer match. For others, it is painful because of the complexity. Yet many others (myself included) go through the motion year in year out without giving it much thought.

So here is an attempt to deconstruct the process.

(update: this was first published in 2016 and has been updated for 2024)

1. Do I need to pay Income Tax?

You’ll need to pay income tax if:

- received more than S$22,000 in taxable income for the year 2023,

- your self-employment net profit is above S$6,000, or

- you’re a foreigner who derives income from Singapore

According to Inland Revenue Authority of Singapore (IRAS), the rates are progressive and high income earners are taxed more as a proportion of their income.

The actual rates for YA2023 are as follows;

| Chargeable Income | Income Tax Rate (%) | Gross Tax Payable ($) |

|---|---|---|

| First $20,000 Next $10,000 | 0 2 | 0 200 |

| First $30,000 Next $10,000 | – 3.50 | 200 350 |

| First $40,000 Next $40,000 | – 7 | 550 2,800 |

| First $80,000 Next $40,000 | – 11.5 | 3,350 4,600 |

| First $120,000 Next $40,000 | – 15 | 7,950 6,000 |

| First $160,000 Next $40,000 | – 18 | 13,950 7,200 |

| First $200,000 Next $40,000 | – 19 | 21,150 7,600 |

| First $240,000 Next $40,000 | – 19.5 | 28,750 7,800 |

| First $280,000 Next $40,000 | – 20 | 36,550 8,000 |

| First $320,000 In excess of $320,000 | – 22 | 44,550 |

Based on the table, an individual with $30k of chargeable income will pay $200 (0.67%), while someone earning $1 million will have to stump up $194,150 (19.4%) for IRAS.

Sounds about fair.

Do note that from YA 2024, tax rates will be revised for those with higher income! You can view the YA 2024 rates here.

2. NFS. AIS. NOA. What are they in plain English?

First of all, it helps to understand how the process works.

IRAS needs to determine how much money we have made in 2023 so as to send us an income tax bill.

What is NOA?

The ‘filing’ of tax returns is essentially us telling IRAS how much we have made and what kind of rebates we qualify for. After this information is made known to them, they will then send us a tax bill before September. The Notice of Assessment (NOA) refers to our tax bill.

What is Auto Inclusion Scheme (AIS)?

Rather than have individuals telling IRAS how much we have made, IRAS has gone to the employers direct and have them provide salary information. Participation in the Auto Inclusion Scheme (AIS) is compulsory for companies with more than 10 employees.

If your employer is under the AIS (search here if you are unsure), you do not need to provide your income figures. IRAS already knows how much you earn.

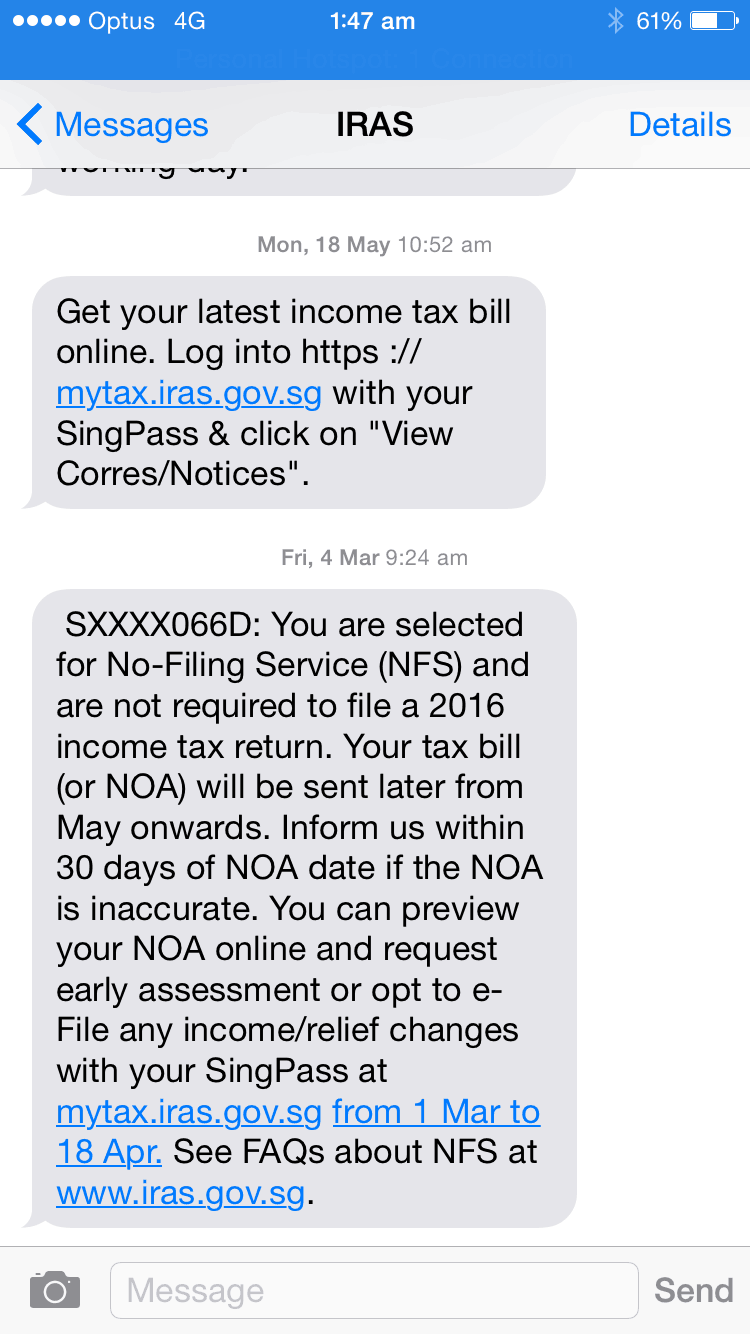

What is No-Filing Service (NFS)?

Because IRAS knows exactly how much you earn, and they also know from your past records that you do not have other sources of income, they have gone one step further and initiated the No-Filing Service (NFS). There is no action required on your part if you have been selected to be part of the NFS.

If you have been selected for NFS, you would have received either a mail or an SMS informing you of that. You do not need to lift a finger in this case, IRAS will send you the NOA or tax bill to you automatically, from end April onwards.

3. Must I File Income Tax in Singapore?

If you have received notification asking you to file, you have to file.

This is regardless of whether you have received income in the previous year, or if your employer is part of the AIS. IRAS just wants to hear from you I guess.

If you have received notification asking you not to file, you do not have to file:

If you are in doubt, just log in to IRAS and have a look see.

4. Am I entitled to Tax Relief in Singapore?

Not every single cent of your income is taxable. There is an entire range of tax reliefs available for the taxpayer to reduce his or her taxable income. You can view the full list of tax reliefs via IRAS website here.

The one most applicable to all is CPF contributions. For every dollar one earns, 20 cents goes into our CPF account which will provide for our retirement. CPF contributions are non-taxable. The amount you contribute to your CPF will be excluded from your income by IRAS.

Here’s an example:

For myself, I am entitled to tax rebates on my two kids. In total, they bring down my taxable income by $8000 (in 2017).

Other reliefs worth mentioning include:

- Personal Income Tax Relief, where you can get Tax Relief off your personal income subject to an overall relief cap of $80,000 per YA,

- Life Insurance Relief, where the amount spent on life insurance premiums entitles you to a deduction,

- CPF Cash Top Up Relief which operates similarly to the Life Insurance Relief.

For someone whose taxable income is $80k a year, he would be paying $3350 in tax. Assuming he does a CPF cash top up of $8000 which is the maximum permissible, he would have reduced his taxable income down to $72k, bringing his tax bill down to $2790 for a savings of $560. For many, this is a good way to ‘reallocate assets’ and save on taxes.

For individuals who are required to file, it is important to include the correct reliefs in your tax returns.

For those who are not required to file their returns, you are required to inform IRAS of any discrepancies upon receipt of your NOA.

5. I hear of donations being tax deductible. How do I make use of that to reduce my tax bill?

Every dollar you donate to a registered charity (also known as IPC, Institute of Public Character) reduces your taxable income by 250%, till 31 Dec 2026.

In other words, if you were to make $3000 in donations in 2021, your taxable income will reduce by $7500. If your taxable income is more than $320k and you fall into the highest bracket, this $7500 reduction will see you paying $1500 (20% of $7500) less to the taxman. Hence, your ‘outlay’ on the $3000 donation is effectively only $1500.

For the vast majority of salaried employees who fall under the more ‘normal’ tax brackets, the savings will be lesser. It is possible to drop a bracket via donations, but because of our progressive tax structure, it is impossible for the savings to exceed the actual donation amounts.

6. Capital Gains, Dividends and Rental Income. Are they taxable?

There is no Capital Gains Tax in Singapore. Retail investors do not need to declare profits from the sale of shares. Neither do they need to do so for properties (small caveat, unless the taxman labels you as a property trader).

Dividends are handouts by companies that report profits from their operations. In computing their profits, companies would have taken into account their revenue, expenses and tax payable. Hence, dividend are derived after tax considerations and are deemed to have been taxed at source.

There is no dividend tax nor requirement for retail investors to declare dividends received in filing their tax returns either.

Rental income is taxable and it is the responsibility of the owner to accurately declare. If you are a property owner deriving rental income from your property, there is a range of expenses that will qualify for rebates as well. It pays to review them and ensure that they do not go to waste.

You can refer to this IRAS page for other sources of taxable incomes.

Conclusion

For years I have not given much thought to income tax issues. I used to see it as a chore. (I still do actually).

But in preparing for this article, I have spent some time reviewing the IRAS website and reading recommendations. I come to the conclusion that taxes (and all the other aspects of personal finance and investing) is one’s own responsibility and that no one would or should care for your money issues more than yourself.

The points which I felt were useful and I wished someone had told me before, I have raised them in this article. If there is anything else you feel is important, do give me a shout out.

Happy Filing!