In September 2016, Schroders surveyed 20,000 retail investors in 28 countries, including 500 investors from Singapore. One of their biggest finding is that investors are overly optimistic about their expected returns.

According to the survey, the average investor in Singapore is expecting 9.2% returns per year! That is way too unrealistic given the low interest rates environment in the current market.

The Risk Free Return (Benchmark return)

When we talk about returns, it is always associated with the risk of investment. The higher the risk, the higher the potential returns that you can expect.

In the Singapore context, the risk free return is yield derived from Singapore Government Bonds (SGS). They have a risk rating of triple A which is considered risk free. The returns for Singapore Government Bonds are as follows:

Source: SGS website as of 9th Oct 2016

There are a few things we can take away from the table above. Firstly, the longer the term, the higher the returns. This is to compensate the bond holder for the longer holding horizon.

Secondly, the returns are lower in 2016 as compared to 2015. This is in line with the lower interest rate both globally and locally. Finally, the returns are ‘only’ 1.39% for a 5 year Singapore government bond. If you desire higher returns than 1.39% over a 5 year investment horizon, you will need to take ‘some’ risk. In this article, I will be sharing the risk and returns for the typical investments in Singapore.

Disclaimer: The following information is based on historical returns and does not indicate future performance.

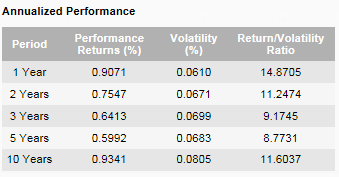

Money Market Fund

The objectives of a money market fund is to invest in highly liquid assets and give potentially higher returns than the savings rate with no lock in period. One of the biggest money market fund in Singapore is from Phillip Capital. Investing in the fund is easy. All that is required is an account with POEMS. Below are the returns reported in the fund fact sheet:

Source: Phillip Capital MMF as of 9th Oct 2016

Risk

The fund is still subject to investment risk. However, at 0.0805% volatility over the past ten years, the risk is definitely on the low side.

Fixed Deposit

A fixed deposit account is the other low risk instrument. It is also the most familiar and the most widely used among retail investors. The returns of fixed deposit varies from one bank to another. Moneysmart.sg has an online platform to compare all the fixed deposit schemes in Singapore banks.

From the website, a 5 year fixed deposit promises approximately 1.2%. Do take note that all the banks have different tiers for different investors. If you are in the priority banking or private banking tier, you should get higher returns.

Risk

For bank savings in Singapore, only the first $50,000 is protected under deposit insurance scheme. In the event of insolvency of the bank, you may loss some of the savings.

Endowment

One of the main purpose of endowment plan is for wealth accumulation. Some of them do provide some protection on the life assured. The returns of endowment plans vary widely from one to another.

On top of that, typical endowment plan comes with guaranteed and non-guaranteed return. I have written an article on everything you need to know about endowment plan. I have also created a calculator to determine the returns of endowment.

Typical returns for a 5 year endowment plan is about 2.25% a year.

Risk

In my personal opinion, Endowment plans should provide higher guaranteed maturity value than the total investment amount. If that is the case, the risk of the investment is that the endowment provider does not honour the guarantee due to insolvency. Again, certain portions of the endowment investment is protected under Policy Owners’ Protection Scheme

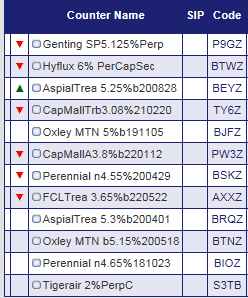

Corporate Bond

Corporate bonds are the other typical investment in Singapore. The list of retail corporate bonds are as below:

Source: SGX retail bond as of 9th Oct 2016

You can see that the returns from corporate bonds vary quite a fair bit. This is because different companies are exposed to different levels of risk. The highest coupon rate is from Hyflux 6% Perpeptual Securities and lowest is 2% from Tigerair Perpeptual Bond.

The number of corporate bonds available to retail investors are somewhat limited. However, there are many more corporate bonds available for Accredited Investors. These bonds are traded over the counter and are not listed on SGX.

The risk/returns principle remains unchanged – the returns you will get depends on the risk of the company that you are investing in. Generally returns range from more than 5% for higher risk bonds and less than 3% for the lower risk offerings.

Risk

In the event that a company defaults, an investor may loss the entire investment amount. The most recent example is the case of Swiber who defaulted on their bond offering. Generally however, if an investor is prudent with the analysis or when he or she chooses to invest in bonds via a bond fund, the risk is about 20% of volatility in term of the bond price.

Equity Market

Equity investment is one of the most common form of investment in Singapore. When we speak about market returns, we always refer to the benchmark STI ETF. Below is the returns of the SPDR STI ETF:

Source: SPDR STI ETF as of 9th Oct 2016

As you can see, the returns inclusive of dividend is just 2.39% per annum over the past 5 years and 4.36% per annum over the previous decade. It is not a very fantastic number on all accounts. However, the potential returns could be higher if equities were to perform better in the future.

Risk

Investing in equities is considered high risk. During the global financial crisis, the Singapore Index dropped by more than 50%. If you intend to invest in equities, be willing to accept that your portfolio might lose up to half its value during a market crash.

Individual Equity

Given the relatively lower returns from the equity market, one can try to pick individual stock in order to outperform the market. However, the range of returns is very dependent on the investor’s ability. One of the greatest investor of all time Warren Buffett is able to generate about 23.9% a year, The Dr Wealth CNAV Portfolio generated 10% to 15% per year.

Source: CNAV Portfolio Performance as of 31st Oct 2017

Risk

Again, the equity market considered a high risk venture. Picking individual stocks is even riskier than investing in the entire market. If you pick the wrong stock, you may loss all your capital.

Alternative investment

Other than all these traditional investments, there are many other alternative investments like Gold, commodities, property, futures, options, bitcoins and private equity.

The risk and returns vary widely and is highly dependent on the timing of investment and the skill of the investor.

Total Portfolio Management

I always advocate a balanced approach to one’s investments. One should use various financial instruments for wealth accumulation to achieve better risk adjusted return.

The questions of how much to allocate to each instrument and how long to hold on to each investment depends on the individual’s risk appetite and the objective of the investment.

If you wish to review your investment portfolio, do drop me an email at louis@drwealth.com

Image Source: TimesHigherEducation