“I will buy stocks when the market crashes.”

Have you heard this before?

Such expressions or variations of it can be heard commonly while the stock market was performing.

However, you would rarely hear investors say that anymore when the stock market tanked, like what is happening now.

Most would share their concerns why the markets are going to get worse or why this time is different because of inflation and rising interest rate; or that recession is coming and would sink stocks.

This is normal as we are only humans and we allow fear to override logic. We spooked out when we see stock prices plunging endlessly and our portfolio value erased in quick time.

Hence most would stay out of the markets and not invest, contradicting the initial plan of buying during a market crash.

Buying when markets are down

I hope that showing you some numbers would help to clear your head.

Want more than 10% per year returns?

One trick is to buy when the markets were down by 30% from the highs according to Nick Magguilli, who documented the study in his book “Just Keep Buying”. Here’s an important chart from the book:

Interpreting the chart, it means that more than half the time, you would have achieved 10% per year return or more when you buy and hold the stocks till the next market. Else you still get a good chance of achieving 5-10% per year.

Only less than 10% of the time you would achieve below 5%. In fact, you would not have lost money in any of these cases.

As of now, S&P 500 and Nasdaq Composite were down 25% and 35% from their peaks respectively. While we don’t where the bottom will be, the odds are already in our favor after such declines.

If you are convinced that you have to invest, let’s talk about how to invest conveniently.

DBS digiPortfolios

You might not have the confidence to do your own investments or have the time to monitor the markets. This is why DBS offers digiPortfolios which you can conveniently invest on the digibank app.

DBS digiPortfolio is not your regular roboadvisor. The portfolios are managed by the DBS Investment Team who incorporates DBS Chief Investment Office’s views on asset allocation and rebalancing, thereby adding expertise and experience on top of a digital solution.

DBS has enhanced their offerings with two more portfolios, so there are now four for you to choose from:

- Global Portfolio

- Asia Portfolio

- Income Portfolio (new!)

- SaveUp Portfolio (new!)

If you are convinced that it is now opportunistic to buy stocks and want higher returns, go for Global or Asia Portfolio.

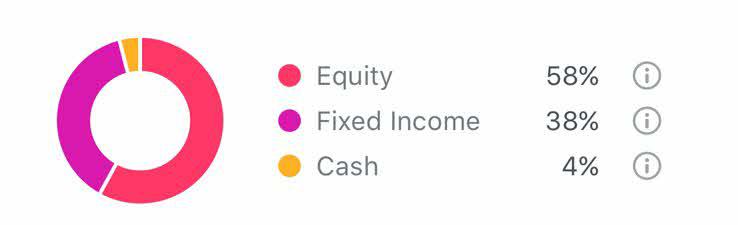

They both have higher allocation to stocks at the time of writing – Global and Asia portfolios have 53% and 58% equity exposure respectively. But you can adjust the allocation using 3 different risk options – choose a higher weightage to stocks if you want higher returns or a higher weightage to bonds if you want less volatility.

Global Portfolio allocation

Asia Portfolio allocation

The Global Portfolio gives you exposure to US, Europe and Asia stocks and bonds by using Irish domiciled ETFs – they reduce the dividend taxation for foreign investors.

The Asia Portfolio gives you exposure to Singapore, India and China stocks. It also balances the equity exposure with Singapore government and corporate bonds.

As we do not know where the market bottom is, one good approach is to do dollar cost averaging – invest a small amount each month so you can average out your purchase prices.

The good thing about digiPortfolios is that you can launch the portfolios with a lump sum first – US$1,000 for the Global Portfolio and S$1,000 for the Asia Portfolio, and thereafter invest in smaller amounts starting from US$100/S$100 per month.

This makes regular investment ‘affordable’ for most investors and able to take advantage of the market volatility to buy more when prices are down.

If you have a smaller appetite for volatility, the two new portfolios might be more suitable for you.

Income Portfolio

As the name suggests, the Income Portfolio focuses on producing regular cash payouts to investors. The other portfolios do not have this option as all dividends and interests are automatically reinvested.

Of course, you can choose to reinvest the payouts to compound your returns with the Income Portfolio too. But I would think this Portfolio is most useful to those seeking regular cash flow.

The Income Portfolio aims to pay out 1% each quarter or 4% in a year. Such payout level should be sustainable and its predictability is a godsend for cash flow planning.

Considering that interest rate may rise further, a better way is to do dollar cost averaging as it would allow you to buy at lower prices and get higher yields in the future.

One psychological benefit of seeing the cash going into your bank account is that it can help soothe your nerves when the market gyrates up and down. It may help you stay invested.

Besides the yield, another tangible benefit is that I expect capital gains in the future when the market recovers, as shown in the stats in Maggiulli’s study above.

You might be curious how the Income Portfolio generates the cash payout.

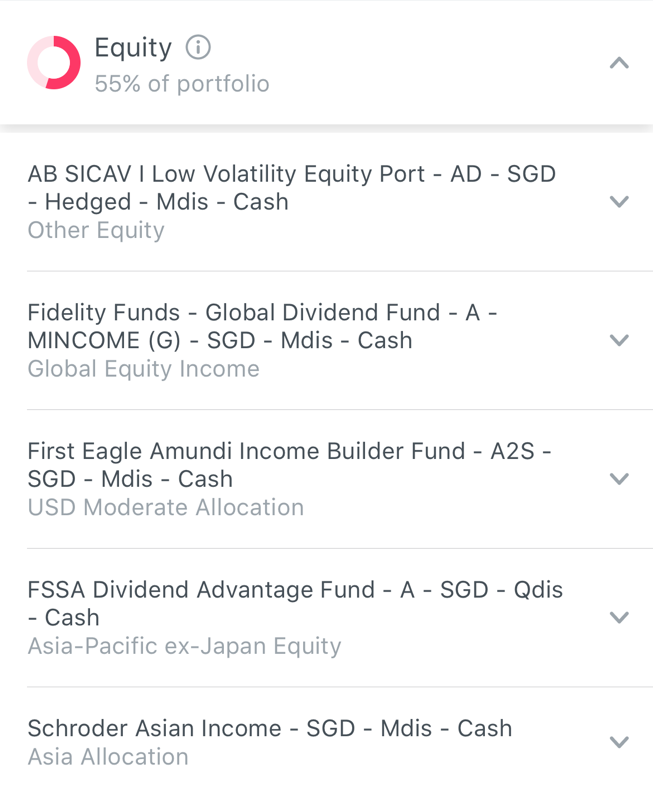

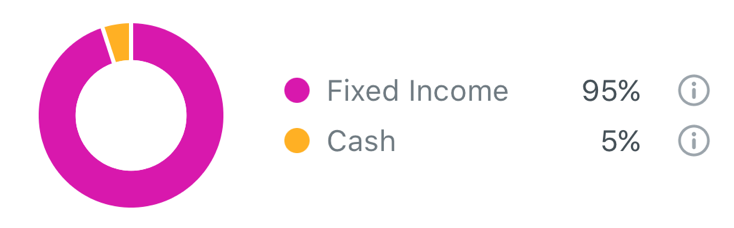

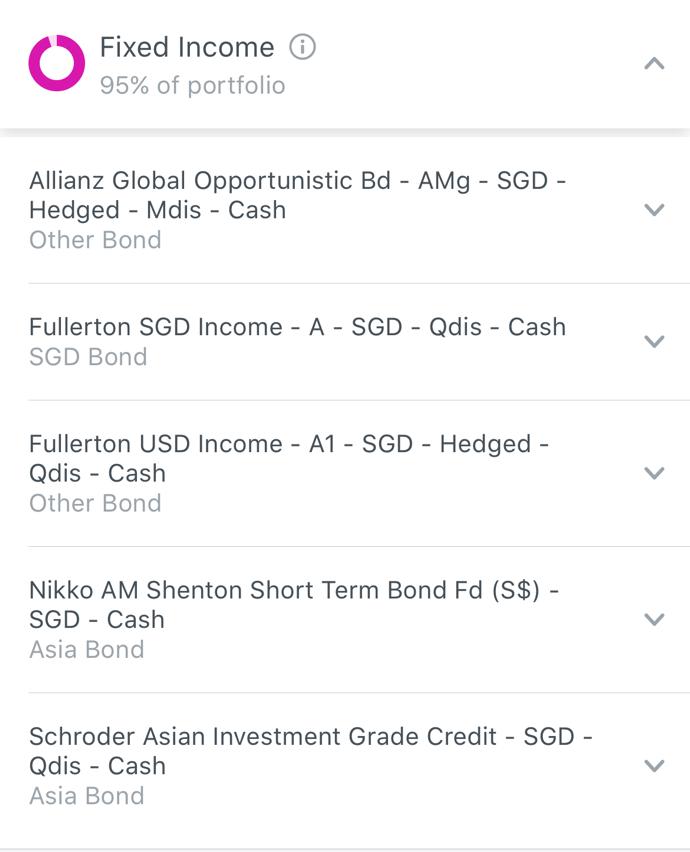

The answer lies in holding dividend paying equity funds (55% allocation) and interest payments from bond funds (40% allocation).

The Income Portfolio is constructed by a mix of income-producing unit trusts as shown in the lists below.

But if you are not ready for a large stock market exposure even after I showed you the advantageous odds, you can opt for the SaveUp portfolio that is relatively less volatile.

SaveUp Portfolio

The first unique feature of SaveUp Portfolio as compared to the other portfolios is its zero allocation to stocks. It is mostly into bonds.

The portfolio is made up of 5 bond funds. They are investment grade bonds with a mix of short and mid-term tenures. So one can conclude that they are relatively safe.

A key point about bonds is that their prices get pushed down as interest rates goes up. And interest rates are expected to rise further so one might be concerned of further capital loss if invested.

My thinking is that bond prices have already been beaten down and we wouldn’t know when the rate hike would stop and at what levels.

The principle is similar to stocks – if the prices are down so much, the chances of a rebound would increase and it makes sense to start buying at some point in time.

We wouldn’t know where the bottom would be and you don’t need to buy at the exact bottom to make money. Again, dollar cost average.

Even though most would look at the bond yield for such bond-focus portfolio, I think the biggest benefit is the capital gain that may come later, should interest rate stabilize or even get cut in the future.

The second unique feature is its low management fee of 0.25%, which is lower than the 0.75% for the other digiPortfolios.

This makes sense considering that the potential returns are lower due to their lack of exposure to stocks. The fees are kept at a minimal level to ensure returns remain meaningful to investors.

The third unique feature about SaveUp is that you can start with just S$100. This is the first time DBS digiPortfolio is lowering the entry level to a much lower sum compared to the rest of the digiPortfolios. This makes it easier for investors who prefer to start small to begin their investing journey.

Here is a quick comparison between the two new digiPortfolios:

Would you invest now?

Buying stocks when the market crash sounds nice when the market is stable but scary to do when the crash actually happens. The falling markets have already spooked investors.

But it is important that we do not allow the fear to get the better part of us. Using historical market statistics to identify our odds of investment success can ground us with logic.

With DBS digiPortfolios, you can now invest easily and conveniently. The four portfolios – Global, Asia, Income and SafeUp have distinct objectives, allocation and features. You should be able to find one that fits your needs and risk profile.

You can find out more details here.

This article is written in collaboration with DBS. The opinion is mine and not reflective of DBS or Dr Wealth. The views are generic and do not consider your unique situation. Seek professional advice if you aren’t sure how to decide on your investments.

Disclaimers and Important Notice

- This article is for general information only and should not be relied upon as financial advice. Any views, opinions or recommendation expressed in this article does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

- This advertisement has not been reviewed by the Monetary Authority of Singapore.

- It is provided in Singapore by DBS Bank Ltd (Company Registration. No.: 196800306E), an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore

- The information and opinions contained in this article has been obtained from sources believed to be reliable, but DBS makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose.

- This article is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.