Two days ago I wrote about Medishield Life and how it is a definite improvement over the current Medishield scheme. I also noted that while comprehensive, there are still certain aspects of hospitalisation and healthcare that is left exposed.

Private Integrated Shield

To ‘enhance’ our Medishield Life coverage, we turn to the Private Integrated Shield. It is important to note that while Medishield Life is a CPF Board administered scheme, the Private Integrated Shield is underwritten by private insurers. The premiums from both schemes are deductible from Medisave.

To begin with, let us examine some common misconceptions about the PIS.

- Medishield Life will cover all my hospitalisation expenses, I do not need Private Integrated Shield

- Private Integrated Shield is duplicate coverage. I will end up paying double for Medishield Life and Private Integrated Shield

- I will not benefit from Medishield Life if I buy Private Integrated Shield

Firstly, as explained in the previous article, even though there are increased benefits for Medishield Life, there is still no full coverage by Medishield Life. Co-insurance and deductibles are two components borne by you if you are admitted to hospital.

Secondly, Private Integrated Shield plan is packaged together with Medishield Life. Do not confuse the single premium you are paying as a duplicate. In actual fact, the premium you paid for the Private Integrated Shield plan is divided into two portions. The first portion of goes to CPF Board for Medishield Life coverage while the remaining is directed to the private insurer. Here is a graphical representation.

So, if you purchase the Private Integrated Shield plan, you will not be making duplicate payment for Medishield Life and you will be covered under Medishield Life as well.

Should I get Private Integrated Shield?

Medishield Life only covers basic hospitalisation expenses. Personally I would prefer to get myself covered with Private Integrated Shield. There are three reasons why.

Hospitalisation plans give the highest coverage per dollar of premium paid, especially so when it is a Government sanctioned scheme.

Without Private Integrated Shield, Medishield Life only covers hospitalisation costs of up to B2/C ward. If I choose to seek treatment at a private hospital or stay at a higher ward class, the additional costs incurred will be my responsibility.

Finally, I would not want to worry about the deductibles and the coinsurance components of the hospital bill should I be admitted.

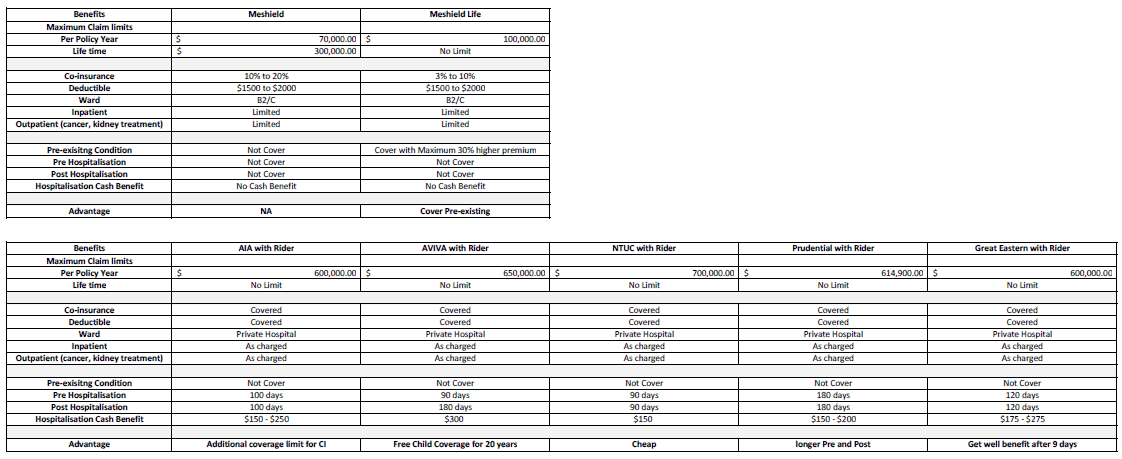

Here are the summary of Medishield Life vs Private Integrated Shield Plan:

And below is the graphical presentation of Private Integrated Shield Plan:

Which Private Integrated Shield Plan Should I get?

Currently, there are 5 Insurance companies in Singapore providing the Private Integrated Shield plan. They are NTUC, AIA, AVIVA, Prudential and Great Eastern.

Each of them comes with different price and different benefits. Which one should you get is very dependent on what benefits do you prefer. For example, AIA provides additional coverage for critical illness, while AVIVA throws in free child coverage for 20 years and NTUC has chosen to compete on price. To cut long story short, I have summarised all of them in the following table.

How much do I need to pay for Private Integrated Shield Plan?

The Ministry of Health has provided an easy use calculator to show exactly how much each individual needs to pay for Medishield Life coverage. The premiums are intentionally kept affordable for the majority of Singaporeans and the entire amount can be deducted through Medisave.

We are also allowed to use Medisave to pay for the approved Private Integrated Shield Plans subjected to a maximum withdrawal limit. Hence in purchasing the Private Integrated Shield, there will always be a cash top up component involved.

With the implementation of Medishield Life and the Private Integrated Shield Plans, the premiums paid will increase. CPF Board will also be increasing the annual withdrawal limits so that the cash outlay remains affordable.

As you can see, the cash outlay remains close to the region of $500 per year all the way till 50 years of age. These numbers are based on the private hospital plan for each private insurer. They become lower if we are willing to forgo private and stick with public healthcare.

For more information on Medishield Life and Integrated Shield Plans, do check out the Medishield Life site here. Alternatively, should you have more questions, do leave your comments below or contact me via louis@bigfatpurse.com

Since there will not be any additional benefits for those who have insured with comprehensive Private Integrated Shield Plans (assuming no pre-existing illness), why there is mentioned about additional premium once the Medishield Life is effected, bearing age adjustment?

Put it another way; the additional benefits provided by Medishield Life will be offset by the reduced benefits of the Private Insurance’s portion, for the same total coverage. Hence, there should not be any additional premium payable as a whole. Am I correct?

Hi Ing Hwa,

The additional premium for the private integrated shield plan is because of the increased in premium from medishield to medishield life.

I do agree with you for your second statement. I have actually posted this question to the private insurers. The answer they gave to me is because the reduced benefits from private insurer portion is offset by the increased in medical inflation. So the premium for the private insurer portion remain the same. This is the same for all 5 insurance companies that provide private integrated shield plan.