Associates, Joint Ventures and Subsidiaries are known as intercorporate investments.

Just like individuals, companies can invest in other companies and own them legally.

Each of the incorporate investment has a different treatment in the financial statements and it is important for investors to understand the differences and how it can impact the figures.

Subsidiaries (usually more than 50% ownership)

A company is known as a subsidiary when the parent company has a controlling stake, which is usually indicated by more than 50% ownership. The acquisition method is used to account for the subsidiary’s finances.

Under the acquisition method, the financial numbers of the subsidiary will be combined with the parent’s financial statements. You would notice most of the financial statements have two main columns, Group and Company. Group refers to the combined accounts of the parent company and her subsidiaries while Company only includes the parent company’s finances.

This is the reason why the statements are usually titled as ‘Consolidated‘. The subsidiary is accounted in a way that the parent company has acquired it.

There is another important implication about the acquisition method. Not all the subsidiaries are fully owned by the parent company. For example, a parent company may only own 60% of a subsidiary, but 100% of the subsidiary’s finances are combined into the group numbers of the parent.

The remaining 40%, not owned by the parent company, will be reflected as non-controlling interests.

If the non-controlling interests is large, the company’s balance sheet would be fictitiously higher than it appears to be.

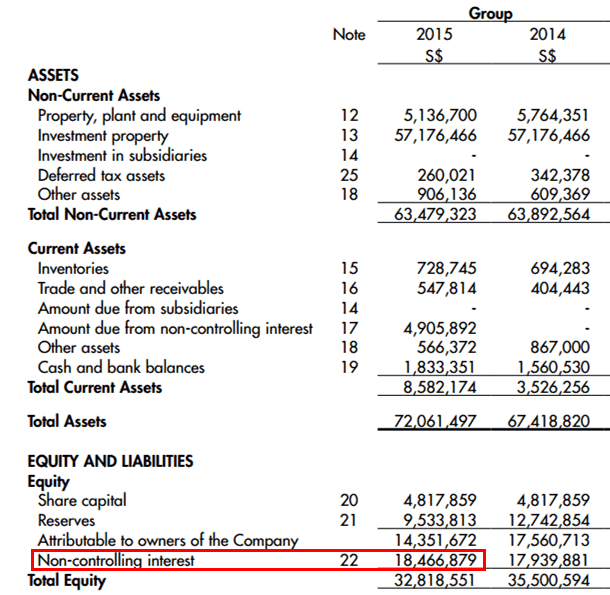

An example would be Mary Chia which is listed on the SGX.

The Total Equity was $32m while the non-controlling interest was $18m. The actual equity for shareholders of the company is only $32m – $18m = $14m!

The company may seem bigger than it is when the non-controlling interest is substantial.

Associates (usually 20-50% ownership)

When Company A is described to have significant influence over Company B, B would be known as an associate and would be accounted using the Equity Method into A’s financial statements.

If company A owns 50% of Company B, the latter is known as a Joint Venture. If the ownership is between 20% to 50%, Company B would be known as an associate company to Company A.

For equity method, the cost of investing in B will be recorded as a non-current asset in the balance sheet of A.

Thereafter, the proportion of earnings of B will be recognised in the income statement of A, and also increase the non-current asset (Investment in Associate) in A’s balance sheet.

If B distributes dividends, A’s non-current asset reduces by the proportionate amount as it is taken as a return of capital.

If B makes a loss, it would reduce the earnings of A in the income statement and also reduce the non-current asset in A’s balance sheet.

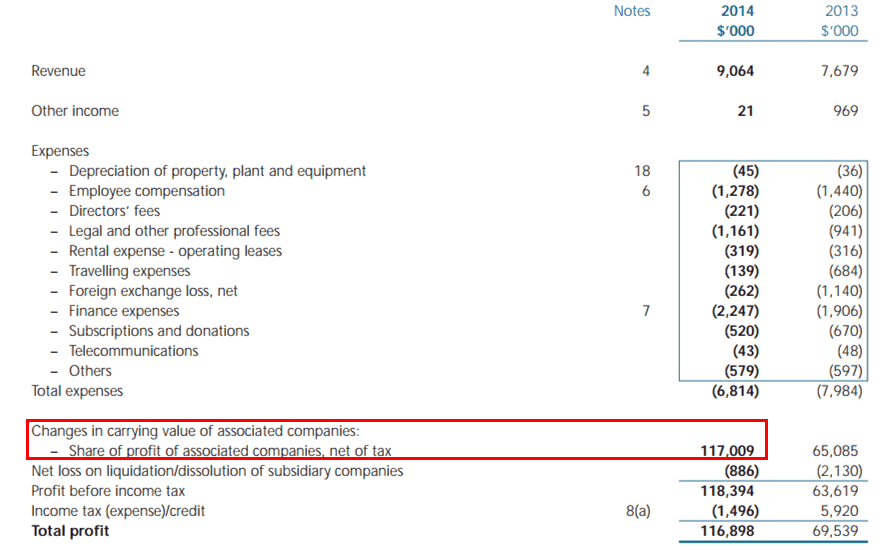

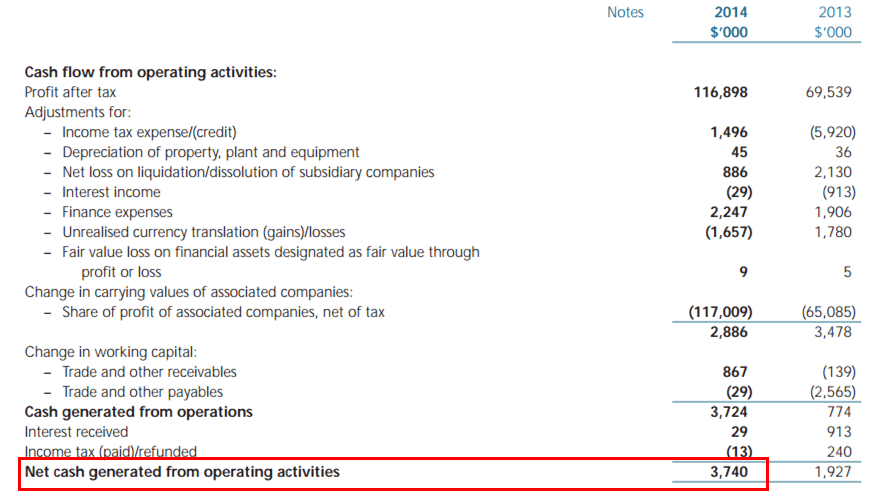

An investment holding company would possibly have more investment in associates than other kinds of companies. Such company may have high profits but low operating cash flow. This is because the equity method would recognise the earnings of the associates in the income statement but excluded in the cash flow statement, especially when the associate company does not pay out dividends.

In this case, Operating Cash Flow or Free Cash Flow may not be applicable metrics to value the company.

An example is Pacific Century listed on the SGX:

Financial Assets (usually less than 20% ownership)

Lastly, if Company A owns less than 20% of Company B, B would be recorded as a financial asset in A’s balance sheet.

The financial assets are then sub-categorised into Held-to-maturity, Fair Value through profit or loss, and Available-for-sale. Held-to-maturity assets are investments with determinable payments and fixed maturities such as bonds.

As for the other two, they have different treatments in the income statement but let’s not go to the details as the final profit of the company would be similar.

The assets would be recorded at fair value in the balance sheet and any gains and losses would be recognised in the other comprehensive income, but will not attribute to earnings of the company until the investments are sold.

Below is a screen shot of Hotung’s balance sheet, which the company is listed on the SGX, has a significant investment in financial assets. The asset value of Hotung is highly dependent on the performance of the fair value of financial assets, and it is also tedious to evaluate and keep track of the fair value of the individual investments.

Conclusion

Here is a summary:

| Ownership Level | Accounting Treatment | |

|---|---|---|

| Subsidiaries | More than 50% | Acquisition Method |

| Joint Ventures | 50% | Equity Method |

| Associates | 20% to 50% | Equity Method |

| Financial Assets | Less than 20% | Fair Value |

Most listed companies have subsidiaries, associates or investment in financial assets. Hence, investors must have a good understanding how these investments, based on accounting rules, would contribute or affect the earnings and equity of the parent company.

Some errors.

OCI is not earnings

Held to maturity are not bonds. They are not the same.

Bonds. An be AFS or held for trading too.

Classification is based on level of control rather than % ownership. % ownership is only evidence of control.

Please do your due dilligence before posting…

Thanks for pointing out.

Amended the article to make it clearer.