Some weeks ago, I compared the “returns” of Term and Life Insurance. The results show that Term tends to outperform Life most of the time. You can read about the comparison here.

I have received some comments about Life Insurance being able to provide cash value while Term Insurance has none. Also, Life Insurance allows you to pay the premium upfront and you will be covered for your whole life.

You might also like

In this article, I am going to explain the second part of “Buy term and Invest the Rest” and show you exactly how much returns do you need to generate from a Term plan in order to outperform a Life Plan.

This comparison is done using Term and Life plans from company T. Term coverage is calculated to age 99. Here are the premium amounts for a $300,000 death benefit plan for a male at age 30:

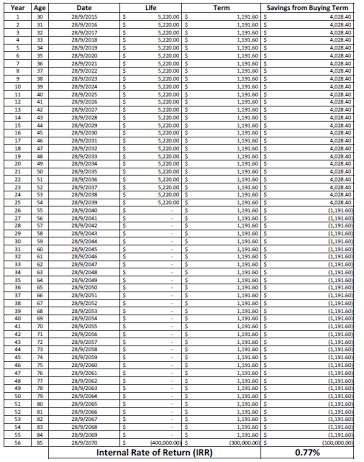

For Term cover to age 99, premium per year is $1191.60 for the entire coverage term.

For Life insurance, premium per year is $5220.00 payable for 25 years only.

Both Term and Life provide the same death benefit. But for the life insurance, there is a non-guaranteed cash value because part of the premium you have paid will go to the participating fund of the company. Assuming a person lives until age 85, life insurance will provide approximately $400,000 death benefit. ($300,000 sum assured + $100,000 cash value with 3.75% participating fund return).

This means that if you buy the Term insurance instead of Life insurance, you will need to generate an extra $100,000 when you are at age 85. So, let us examine that what is the return required to achieve this amount in cash.

- For the first 25 years, you will save $4,028.40 if you choose to buy term insurance instead of life insurance. Assuming this entire $4,028.40 goes into your investment portfolio.

- From the 26th year onwards, this investment portfolio will reduce by $1191.60 yearly. This is the amount needed to pay for the premium of the Term policy. (You would have paid up the Life Plan by then).

- At age 85, this investment portfolio needs to generate an additional $100,000 to make up for the different of death benefit between life insurance and term insurance.

Based on these factors, I have computed the Internal Rate of Return (IRR) of this investment Portfolio as below:

Hooray! The IRR for the investment portfolio is merely 0.77%! In other words, if you can invest and generate more than 0.77% returns per year, you should buy Term Insurance and invest the rest! Yes, there are plenty of investment instruments that you can use to generate much higher returns than 0.77%!

Again, here are some points that you need to take note:

- The IRR result is derived from a $300,000 coverage for a 30 year old male. Different coverage and different ages will yield different results.

- The assumed life span is 85 years old. The results will change for different life span.

- The comparison did not factor in the cost of critical illness rider. Some Life policies are more cost effective when compared to Term Insurance for CI cover.

Disclaimer, this analysis is not to advise you to surrender your life policy and switch to a term policy. Surrendering a life insurance policy always comes with a cost, you should check with your financial advisor before you make any decision.

Do drop me an email at louis@bigfatpurse.com if you have any questions.

Comments 1