On Tuesday 15th March 2016, MOH has announced that private insurers will release Standard Integrated Shield Plans (Standard ISP) starting from May this year.

This is a new initiative introduced by MOH. It will help those who wants to have better coverage than what basic Medishield life can provide, but yet pay lower premium as compared to the existing Integrated Shield Plan.

Also, as compared to the existing ISP, where coverage varies from one insurer to another, the coverage of standard ISP is identical throughout. This will help the public make easier decisions when it comes to the purchase of ISP.

Previously, I had written two articles about Medishield life and Private Integrated Shield Plans.

What is the main benefits of Standard ISP

The main benefits of Standard ISP are as below:

- Coverage up to B1 ward of restructured hospital. At B1 ward, patients can choose their doctors and enjoy air-conditioned rooms

- No “As Charge” coverage

- No pre and post hospitalisation coverage

- Annual claim limit of $150,000

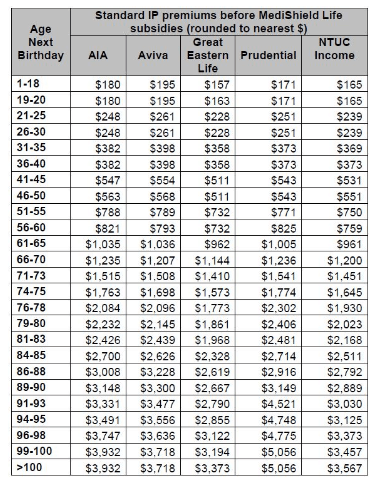

For the full benefit schedule of standard ISP, please refer to the MOH website here.

What should I do?

You will be given an option to change to this new standard ISP as the premiums are lower than for the existing ISP. The following are some points to consider before you decide to make the switch.

- Standard ISP only provide coverage up to B1 ward of restructured hospital. If you are admitted to any ward higher grade than B1, you will have to fork out a certain percentage of hospitalisation expenses.

- No “As charge” coverage for standard ISP means that there is a cap for each expense. For example, you will only be able to claim up to $1,700 per day for room, board and medical-related services.

- Similar to the existing ISP, co-insurance and deductibles are still not covered under ISP.

You need to add a rider in order to have a ‘zero dollar out of pocket’ plan.[2018 update: with the new 5% co-payment rule, you’ll need to pay 5% up-front even if you have a rider to cover your deductibles and co-insurance] - The new standard ISP does not cover pre and post hospitalisation. I find that these two components are very important because in most of the cases, there will be pre-hospitalisation consultation and post-hospitalisation follow up with the hospital.

- Annual claim limit of $150,000 is much lower compared to the existing ISP which range from $300,000 to $700,000

Since the new Standard ISP offers the same benefits, should I change my existing ISP to the insurer that provide new standard ISP with lowest premium?

This is a bit tricky. In theory, if the benefits are the same, of course we will want to pay lowest amount to get the same benefit. However, before you decide to switch, it is important to know if you have any medical condition. A new insurer may not want to cover your medical condition if you switch with the existing medical condition. If you choose to downgrade to a standard ISP within the same insurer, no medical underwriting is required.

My views on the New Standard ISP

For those who want to get better protection than Medishield life but do not want to pay too high a premium for ISP, the Standard ISP will do the trick. It is a timely introduction by MOH.

The number of people falliing into this bracket though, will be a minority. According to MOH, 2 out of 3 Singapore citizen and PR have bought an ISP. Out of them, private hospital ISP account for the majority at 56%. Class A accounts take up another 25%. This means that the majority still prefer the private hospital plan even though the premium is much higher.

I share the same view. I think hospitalisation insurance should be top priority. If you really want to save reduce the premium on insurance, I would rather you save on life insurance, endowment plans or even term insurance. This is because the tendency to claim from hospitalisation insurance is much higher than the other forms of insurance.

Please note that this is only brief summary of ISP, you should check with your advisor before you make any decision.

Hi Louise, good summary! Just one point, in point 3 under “What are the main benefits under Standard IP, I think you meant “need to pay for deductible and co-insurance” rather than “no deductible and co-insurance”. Thanks!

Hi Christopher,

Yes. need to use cash to pay for rider to cover co-insurance and deductible. Thanks for pointing out.