Shanghai Stock Index fell 6.5% yesterday (28 May 2015). The Singapore Stock Market was affected by it but not too much. Despite the general bearishness, one of our CNAV stocks, Fu Yu, ran up 10% on the same day. The bamboo-like growth in small cap stocks have been realised again.

Fu Yu is a small cap stock with $146m market capitalisation as of 28 May 2015.

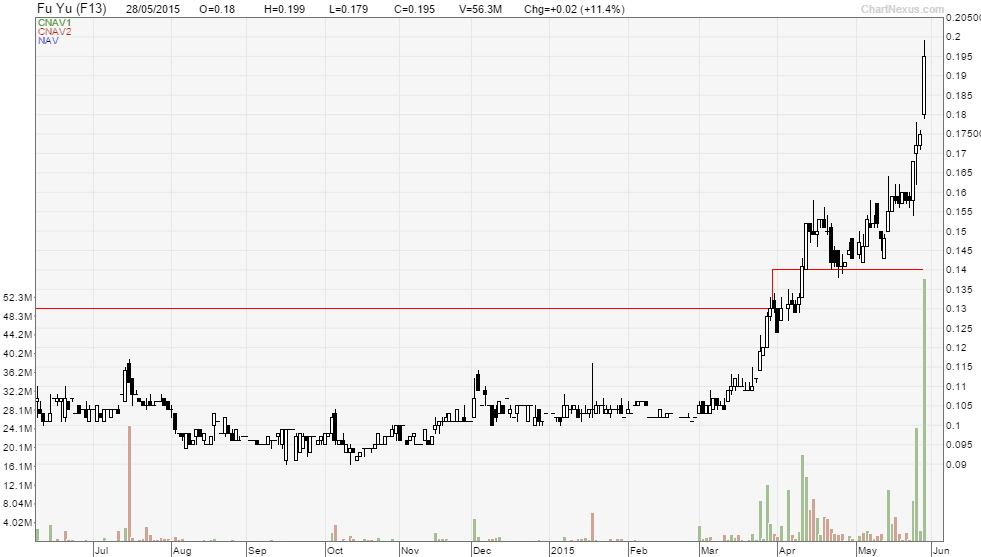

It was one of the fallen and an ugly stock that nobody likes. It is not in the sexiest business and it does not have the highest earnings in the market. We can witness the low liquidity and transaction volume preceding the crazy run up since March 2015. Trust me, most investors will shun this stock and go for something with higher volume, saying this is a value trap.

As counter-intuitive as it is, the best time to buy is when most people are not buying. It is easy to say but very difficult to do. Few want to be the true contrarians in the stock market.

Before the Rise, there was value at a wonderful price

We picked out this stock from our CNAV screen since last year and some of our Dr Wealth Insiders had invested since then.

Based on their 31 Dec 2014 report, 32% of their total assets were in cash, and another 30% in receivables.

The Net Asset Value (NAV) of Fu Yu was $0.24. If we discount receivables by 50%, in case of bad debts, the company is still worth $0.14 conservatively (CNAV).

We have not taken the future earnings of this company and it already gave us a CNAV discount of 30-40% from today’s valuation. As you can see from the stock chart above that there is this red line, and that indicated the conservative valuation of the company and investors had plenty of time and opportunity to get into this low liquidity stock.

Despite the good value, there were common ‘excuses’ why investors should not buy the stock and here they are:

#1 The stock has no liquidity, I cannot buy it and if I do, I would be stuck with the stock for a long time with no one to sell to.

My response to this is: do not look at supply and demand as a static situation.

The levels of supply and demand will change due to myriad reasons. A low liquidity period is a temporal. In fact, it is a sign that the value of the stock has not been discovered by most people yet.

#2 The management doesn’t give dividends.

The last dividend that was given out was in 2005. Most dividend investors would not even want to look at this stock.

Remember that total return is inclusive of both dividends and capital gain from the stock price. But think about this, if you have invested in Fu Yu for 5 years with no dividends, but you have doubled your invested capital through the price gain, you would have made close to 15% per year on the average. This would be much more than someone who have invested for 5% dividends in the past five years.

It is not easy to overcome these ‘excuses’.

The low liquidity and lack of dividends do not give investors confidence. I could tell some of the members who had invested in Fu Yu were feeling uncertain. I have learned over the years that what made you uncomfortable when you invest usually has a favorable outcome.

What gave the phenomenal rise to this ugly stock? Why so sudden? Why now?

Walter Schloss has a 45 years of history buying such low price-to-book stocks. Based on his extensive experience, he said three things will happen when you invest in such stocks:

- Earnings turn around and the stock appreciates significantly

- Someone buys control of the company (buyout)

- The company begins buying its own stock

Fu Yu is a clear case of number 1. The earnings finally turned around and improved after 7 years of consecutive losses in their precision tooling and plastic moulding businesses.

Our good friend, Brian, wrote a very detailed analysis about the earnings in this article.

An analyst from RHB released a very favourable report on 28 May 2015, expecting a 7.1% dividend yield in FY15. I am not sure if this fueled the 56m volume (S$10m) in a day. Here is an extract of their summary of the report:

“We initiate coverage on precision tooling, precision injection moulding and assembly firm Fu Yu with a BUY and a DCF-derived SGD0.30 TP (88% upside). At 1.7x FY15F ex-cash P/E, we believe the stock, which has a high +7% potential maiden dividend yield, is trading at undemanding valuations. With gross margins expected to improve significantly from cost-cutting and restructuring initiatives, we anticipate it to chart a record FY15.”

We do not really care about what the analysts report. Everyone is entitled their own views. But we are more than happy that analysts are picking it up and gathering the interest to realise the value of the stock.

The future of Fu Yu is still an unknown but our members should be waiting to exit at NAV.

Disclosure: I have no position in Fu Yu.

DISCLAIMER: This is an example to illustrate the CNAV investment approach and this information shall not be serve as an investment recommendation nor a financial advice to the reader.

Hi Alvin,

Another brilliant example of the CNAV strategy.

But what if ppl bought into this stock at 7 yrs ago with same CNAV reasoning, but wait till now to hit the returns, would this still be a successful investment?

Note that some companies take a damn long time to realise its value. How is this the time issue being addressed?

Chun Siang,

7 years ago the stock wasn’t undervalued. We need to wait for the price to be below the value of the company to provide sufficient margin of safety before we enter. And we add in a Piotroski F-Score variant to increase the chance of the sustainability of value.

As I mentioned in the article, if you wait for five years to make 100%, you have a CAGR of 15%. Isn’t that worth the wait?