Gone are the days when consumers were content with mass-market products. Growing spending power has seen the demand for premium products take off.

While the “premiumisation” theme has been applied in things like baby products and food before, rising demand for high quality products and services has led to premiumization in other sectors like real estate. Before you know it, you see this trend everywhere:

- More than just an office space: WeWork, a co-working space leasing business, calls themselves a global platform of creators that helps people to create a life, not just a living.

- This is fitness evolved: Peloton, a company selling exercise bicycles with fitness regimens, created “exertainment” (exercise + entertainment)

- Thirsty?: S’well created a brand new category called “hydration” for their humble water bottles.

- No longer just steamboat: Hotpot chain Haidilao added new experience for their customers such as manicures, popcorn and performance during meals.

- Level up: Nestle raised the image of their chocolate KitKat by constantly releasing seasonal regional flavours (ie Matcha & Sublime series).

We are living in a world of premiumization right now. More and more companies are turning towards premiumisation as a way to arrest the declining market penetration and stagnant consumption rates.

For us investors, this could open the door to more investment opportunities in consumer goods and services-driven companies.

However, there is more to it than meets the eye.

Some premiumization strategy could be just a clever story and good packaging. When the dust settles, there will be winners and losers. It is important we stay on the right side of this.

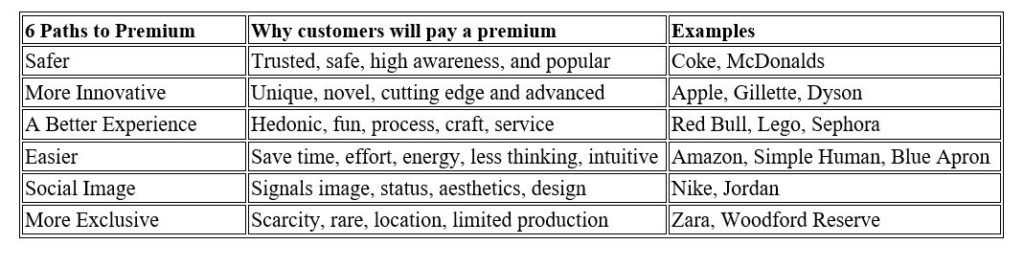

What is Premiumisation?

In simple layman terms, Premiumization is a means to offer higher quality items that consumers value. When this occurs, customers will be willing to pay more for higher quality.

The following are some types of premiumization.

Premium Pricing

Premium Pricing means offering higher value and demanding a premium price in return.

Premium pricing will only work over a longer period of time if a company offers superior value to the customer.

Based on the book “Confessions of the Pricing Man” by Hermann Simon, every business has only 3 profit drivers: price, volume and cost. Thus from the figure below, an increase of 5% in price would increase profits by 50%!

What Should Investors Look Out For?

As mentioned earlier, we’re living in the wild west of premiumization right now.

As new cowboys ride into town, it will soon get over-crowded and only the winners will be left standing when the dust settles.

To help investors understand if a company’s premiumization strategy is working, here are 3 questions to test the quality of the business.

#1 – Has the company done well in terms of sales and profit growth?

In 2016, Okamoto Industries (TYO:5122) launched their Zero One series, the world’s thinnest condom at 0.01mm. That financial year, their profits increased by a whopping 60.6% even though revenue increased by 9.3%.

This is all part of Okamoto’s strategy to have a product differentiation from their peers through innovation. In doing so, they have a premium product on hand which enabled the company to charge a premium price to their customers.

#2 – Does the company enjoy high ROE among its peers?

Warren Buffet often uses Return on Equity (ROE) as his favourite indicator for wide-moat stocks.

ROE shows how efficient the management allocates equity capital to generate returns. Business with high capital over a period of time demonstrates competitive advantages.

Therefore, a stock with high ROE should likely be possessing one or more durable competitive advantages.

#3 – Does the business have a durable competitive advantage?

In the long run, premiumisation will only work if a company offers superior value to the customer. This is usually done through innovation.

In general, innovation provides the foundation for a successful, sustainable premium price position.

Take for example Apple (NASDAQ:AAPL), their groundbreaking iPhone, followed by the implementation of its iOS ecosystem has allowed Apple to transform a technological advantage, which is often temporary, into a long-lasting advantage.

Closing

Consumer growth is one of the world’s most compelling investment themes. Investors can find opportunities in the shifting of the consumer landscape by accessing the “premiumisation” story.

It is important to identify the winners from the bunch and it requires patience, skill and a long-term mindset.

Cheers

Editor’s Thoughts on Finding Investable Companies with Premium Pricing Power

Some of my own thoughts here.

Premium prices in the middle of the bell curve tend to lose pricing power. Premium prices without strong brand belief and fan bases also tend to lose pricing power. Such companies typically die off in a recession and eventually lose their ability to demand top tier prices.

Think of Apple versus say…Sony for example. There’s a reason Apple is consistently able to charge higher prices while Sony’s product prices have consistently languished in comparison – one has a large pool of willing diehard fans willing to wait days outside of a store before a grand opening. The other…does not.

Want to know who has the advantage? Go to any industry and look at who’s able to price their products the highest. See if the profit margins follow the pricing – that is to say, if you’re charging the most in the market, you better be earning the most in the market.

If both checks out, you have yourself a quality company able to consistently charge higher prices whether by the environment (VICOM) or by brand (Apple vs Sony, Coca Cola vs Pepsi) or just sheer dominance (Starhub, Singtel, M1 prior to entrances of competing telcos).

Next ask yourself as Phillip Fisher(Common Stocks and Uncommon Profits) does, whether the company has an increasing and growing pool of users to sell to. A combination of high pricing power and a large pool of people to sell to creates a massively profitable company.

I’d be very willing to own such a company at a fair price given the right conditions (company provides a necessary service, lack of disruption/innovation in the industry for the forseeable future, management owns a healthy chunk of shares so as to be aligned with shareholders in terms of maximizing shareholder value, etc). At undervalued prices, as Buffett says, “the decision should hit you over the head with a baseball bat” – it becomes a no brainer to buy.

Moss Piglet earlier on alluded to the fact that you need to be careful picking the winners from the losers.

For this purpose, I would recommend retail investors only select companies who have consistently demonstrated premium pricing powers along with all the above conditions (inside share ownership, profit aligned w pricing, a growing pool of users to sell to, no disruptions) for at least a decade.

Some helpful ways to mitigate risk is to also check operating expenditures against debt and the ability of the companies to run without debt (Debt below 40% of company equity seems decent, high pricing power companies with an edge would not and should not have problems with cashflow anyway). As we race head-on into 2020 and race against the clock of an inverted yield curve (recession), you want to own the winners, not the losers.

Regards,

Irving