In my previous writeups on potential long plays to capitalize on IMO2020, I focused on shipping companies.

This is only a drop in the ocean as IMO2020 affects all things related to oil. You see – The refining industry is also on the brink of a major shift in the demand structure of bunker fuels.

Refiners are planning ahead and making moves to meet changing product demands brought about by the IMO2020 deadline.

‘SULPHUR is the ENEMY.’

[If I were to write a book about IMO2020, this could well be the title.]

As IMO2020 nears, ports around the world have stopped calling for High Sulphur Fuel Oils (HSFO) as 3.5 million barrels a day of high-sulphur bunkers transitions to the new 0.5% sulphur fuel.

With the imminent collapse in HSFO prices (as well as losing its home in bunkers), refiners also face the challenge in producing IMO-compliant fuels. The global shift towards lower sulphur fuel from January onwards will reduce demand for heavy, high sulphur crudes and more towards light, low sulphur crude.

Already we have started to see refiners increase light crude imports to boost VLSFO supplies (See source here).

Although we have yet to see the sweet-sour crude differentials to widen, PBF’s CEO Tom Nimbley opined that this is because crude purchasing decisions were made months in advance and thus there will be a lag in the physical crude market.

Complexity Matters.

Simple refiners have to decide between switching to purchasing light crude at spot premium or to build expensive secondary units that can further process residual fuel oil leftover from initial refining of heavy oils into high-quality products e.g. gasoline or diesel.

Complexity matters and refiners with deep converging capabilities (like) PBF will have an advantage compared to refiners with less complex systems.

The decline is HSFO prices has also created an opportunity for complex refineries like PBF.

HSFO has backed up into the Atlantic Basin and is seeking an alternative disposition from the bunker market. Because companies are less reliant on HSFO as fuel oil, HSFO is now becoming an option for complex refineries to run as a feedstock in lieu of the more expensive heavier sour crudes.

As mentioned earlier, there is a physical lag in the crude market. As more refineries utilize the discounted HSFO instead of sour crudes, it will also widen the sweet-sour crude spread.

This serves as an additional opportunity for complex refineries to increase utilization to enjoy the higher gross margins in processing sour crudes.

What is Refining?

Refining consists of taking long-chain hydrocarbon charges (a.k.a feedstock) such as crude oil and transforming (cracking) them into shorter-chain finished products such as gasoline and diesel or feedstocks for the petrochemical industry.

You have heard of the big vertically integrated companies such as Exxon Mobil (NYSE:XOM) which supplies their own crude for their refining operations.

Companies like PBF purchase feedstock and sell their finished products to the wholesale market. PBF’s competitors are Phillips 66 (NYSE:PSX), Hollyfrontier (NYSE:HFC) and Valero (NYSE:VLO), amongst others.

The main spread that is the determinant of refining industry margins is known as “crack spread”, which is the difference in the futures market between the price of the primary input (crude oil, fuel oil) and the wholesale price of the finished petroleum products.

Summary of Refining Industry Outlook 2018/2019

The refining sector was in a downturn during 2H18.

The most significant event was the sudden rise in crude oil prices during 3Q18 as oil markets expected U.S.-forced sanctions on Iran that would include a zero-oil export policy.

Refiners were unable to pass along the added costs to its customers as the crude oil price spiked. Mostly due to this event, the RBOB gasoline crack spread plunged from a mid-2018 high in near $17 per bbl to below $7 in end-2018.

OPEC countries and Russia significantly ramped up production to offset the anticipated removal of Iranian oil from the market as well as to take advantage of the higher oil prices.

However, U.S. unexpectedly allowed 8 countries to receive Iranian oil in early November and the formerly-perceived crude oil shortfall rapidly turned into an oversupply glut. Crude prices, which were near $75 bbl at the beginning of 4Q18, plunged below $50 in December 2018.

This should have reversed the tide for refiners, but a strong recovery to wider spreads failed to materialize. Falling automobile sales in China have reduced demand for gasoline. This drop in demand is occurring at the same time that additional refining capacity is being brought online in Asia.

To make matters worse, gasoline inventories surged due to increase in refining activity to produce lighter products like gasoline and increased US light crude production. Worldwide gasoline inventories are above average, adding further pressure on prices.

As a result, refiners like PBF, which derived 88.4% of its 2018 revenues from gasoline and distillates, to struggle.

However, help may be on the way: Since the start of 2Q19, US refiners have cut crude processing, averting a potential oversupply of gasoline and distillates, but worsening the build-up of crude inventories (See source here).

This pushed up refining margin, with gross refining margins for gasoline delivered in January 2020 over Brent at almost $7 per barrel from virtually zero earlier this year.

Although we see from the graph above that stocks have been climbing up again, this could be due to the anticipation of IMO2020.

When IMO2020 kicks in January 2020, it will trigger a conversion to lower-sulphur (i.e., lighter and cleaner) fuels, which should improve refining margins.

This mandate should impact about 3.5 million bpd of bunker fuel, with a net effect of increasing lower sulphur diesel demand by 1-2 million bpd.

PBF is well-positioned for this demand shift, due to the complexity and conversion capacity of its operations.

PBF Energy

PBF Energy (NYSE:PBF) is an independent petroleum refiner and supplier of unbranded petroleum products. It has 5 high-complexity refineries across the U.S. with combined processing capacity of approximately 900,000 bpd.

PBF Energy also owns 44% interest in PBF Logistics, which we believe is a strategic partnership.

PBF Energy: A Pure-Play Refining Company

PBF’s competency lies in disciplined growth through strategic refining and logistics acquisitions, coupled with organic projects developments. Currently, they have a diversified high complexity asset base with 12.2 Nelson complexity.

*Nelson Complexity Index (NCI):

- Measures the sophistication of an oil refinery & usually ranges from 1-20.

- Refineries with higher score means that they have the capability to handle lower quality crude oil or produce more refined products.

June 2019:

- (Competitors’ NCIs): between 12.1 and 9.5

- PBF Energy NCI: 12.8

PBF’s assets are also strategically located near both the East and West Coast of the U.S, very near the busiest cities on both coasts, New York and Los Angeles.

Another edge that sets PBF Energy apart from its large independent refining peers is that the company doesn’t operate any branded retail stations. This means it is the closest pure refining company among largest independents.

Improved Capacity to Take Advantage of IMO2020

PBF’s view is that IMO2020 will generally benefit PBF, and they have made the necessary investments to capture that opportunity.

In their June 2019 presentation, they stated all Capex Spending has been completed for the year and there will be no more required Capex investments.

Restarted Chalmette Refinery

PBF has restarted their idle 12,000 bpd coker facility which is able to convert high-sulphur feedstocks (crude and gasoline) into high-value clean products!

Prices of high sulphur products are expected to fall next year when IMO2020 kicks in and the complex refinery will be able to utilize the discounted high sulphur feedstocks to convert to high-value products.

New Hydrogen Facility at Delaware City

During 2018, PBF decided to proceed with the construction and subsequent lease of a new 25 million cubic feet per day hydrogen facility which is expected to be completed in the first quarter of 2020.

Upon completion, the hydrogen facility will provide the Delaware refinery with additional complex crude processing capabilities.

Acquisition of Martinez Refinery

PBF agreed to purchase the Martinez Refinery from Shell and the deal is expected to close early next year. This refinery is a premier West Coast refinery with a NCI of 16.1.

With this asset, PBF will possess the most complex refining system in the West Coast and will also increase their capacity by 150,000 bpd.

Financials:

(a) Latest Quarterly Report

PBF’s latest quarterly report shows that adjusted net income, excluding exceptional items, was US$80.1mil, or US$0.66 per share, compared to US$1.13 last year.

Free Cash Flow (‘FCF’) came in at US$357mil due to lower Capex. As mentioned earlier, Capex Spending will be low for the rest of the year and this will boost their FCF.

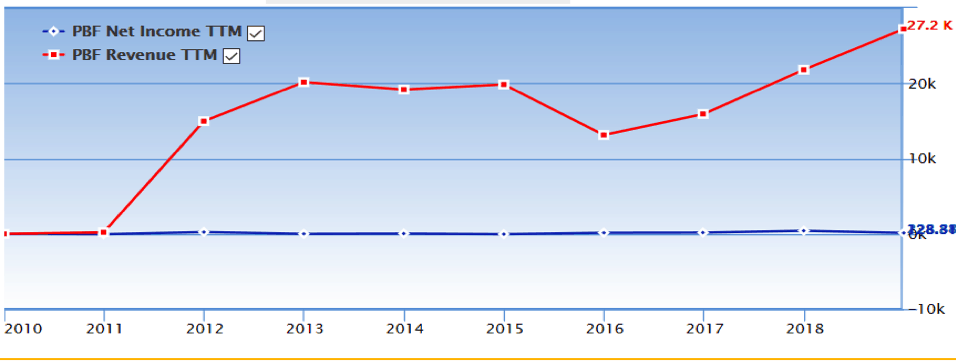

Income Statement:

PBF’s revenue climbed steadily over the years through Acquisitions and Organic Growth!

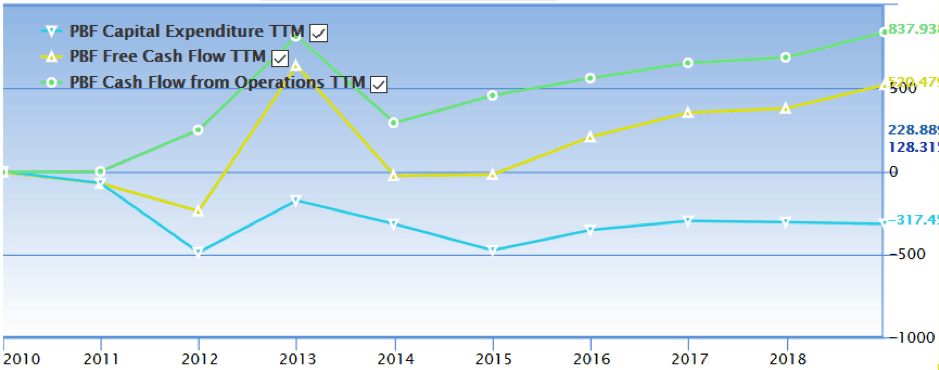

Cashflow Statement

Free Cash Flow is consistent and we also see a healthy increase in their cash flow from operations.

But Capital Expenditure (‘Capex’) is also increasing in tandem with the cash flow from operations.

This is mostly due to an increase in operating capital expenditure from increasing assets’ NCI.

Balance Sheet

The most worrying thing we found in their financials is their High Debt-to-Equity Ratio. While on a decreasing trend, the planned acquisition of the Martinez Refinery will be partly financed by debt as the purchase price is somewhere around US$1B and their Cash-on-Hand is only about US$500mil.

And if 75% of the purchase is financed by debt, this raises PBF’s Debt-to-Equity to above 1.

(b) Valuation

A quick comparison with PBF’s peers suggest that it is fairly valued.

The average PE ratio, if we exclude XOM, is 9.7. The poorer 3Q results have affect PBF’s PE, EV/EBITA and EV/EBIT.

Among the companies, PBF has the highest debt and lowest interest coverage ratio.

Investors interested in PBF should take note of how PBF handles debt.

Even so, its PE valuation is around the refinery sector average of 10x. We think high EV-EBITA reflects the market’s optimism that PBF is poised to turnaround its business and will also be able to extract benefits from the Martinez refinery acquisition.

One of the reasons why we started researching on this company is the fact that there were insider buying activities up until 20 November 2019

(This could also be a confident sign of a stronger FY2020 performance.)

Risks:

(a) HSFO Price

It is widely believed that IMO2020 will drive down demand for HSFO. But this is only a prediction and it may not play out this way. Even if HSFO is shunned by shipping companies, other players such as Power Generation could become a sink for cheap HSFO.

In the longer term, demand for HSFO could even increase if we see a large number of ships install scrubbers and additional refineries upgrade their desulphurization capabilities.

(b) Softness in Gasoline

The price volatility of crude oil, other feedstocks, blendstocks, refined products, fuel and utility services may adversely affect on PBF’s revenues, profitability, cash flows and liquidity.

The softness in gasoline and low-sulphur fuel oil demand could continue if IMO2020 is not as disruptive. Poor economic conditions may reduce demand and build-up of gasoline inventory.

(c) Increased Leverage

As mentioned above, PBF’s decision to buy Shell’s Martinez refinery comes with over-leveraging risks. Even though the acquisition is earnings-accretive once it goes through, further macro-weakness could result in the refinery not meeting its EBITA targets.

Conclusion:

As IMO2020 nears, the refinery sector is starting to see dynamics changing to meet low-sulphur fuel demands. PBF is poised to benefit, due to its complexity and conversion capacities.

A decrease in high-sulphur feedstock prices contributes to higher margins for the company.

They are also able to enjoy higher free cash flow if the crack spread widens, even more so as they do not need any capital investments for the rest of the year.

But the oil and refining industry is highly volatile and numerous factors could affect both the crude and gasoline prices – as we have seen from the past 2 years.

As PBF derives almost 90% of its revenue from gasoline and distillates, any pressure on the crack spreads could cause them to struggle.

We think PBF will stand to benefit if the crack spreads widen as expected due to IMO2020, but we’re concerned about further macro-weaknesses and do not have strong opinions on how the macro-front will play out.

Although huge insider buying activity is usually a sign of vindication, investors who are more experienced with the oil markets could be more informed on how the market will move in the coming months and invest accordingly.

But for Us: Uncertainties in the oil market mean we’re not be initiating a position as of now.

Cheers!

Disclaimer: The Moss Piglet has no positions in any stocks mentioned, and no plans to initiate any positions in the next 72 hours. I wrote this article myself, and it expresses my own opinions.

So here you are – PBF Energy. We chose to go more in-depth because we enjoy giving you a comprehensively holistic analysis so that you can make an informed decision. It doesn’t mean that analysing a ‘potentially-investible’ company is this ‘daunting’.

Because there’s a much, MUCH EASIER way to determine the ‘investibility’ of a company.

Unlike this article which took hours to be written & days to perfect, you’ll know whether you can invest in a particular stock, in just 10 to 15 Minutes – Or Even Less.

Join us at our FREE Stocks Investing 101 Workshop to Learn More. Seats are Filling Fast & this is the LAST WORKSHOP we have for Year 2019.

Register Below Now to Secure Your Seat: